Japan Solar Update: No.142 (Mar 31 ~ Apr 4, 2025)

The 5th Capacity Market Main Auction in FY2024 saw a 240MW bidding capacity for storage batteries, highlighting progress in initiatives for grid-scale storage batteries alongside renewable energy. Area prices (prices by region) have been rising since FY2021, especially in Tohoku and Tokyo, leading to higher overall average prices. Maintenance and management costs for power sources are expected to rise, while electricity demand from data centers and semiconductor factories continues to grow.

Area prices reached their highest levels since the 2nd auction across all areas with particularly significant increases. The rise in area prices and the reduction in deduction rates under transitional measures have led to an increase in the overall average unit price. Looking ahead to future auctions, the cost of maintaining and managing power sources is expected to become more expensive. Consideration will also be given to the status of overseas capacity auctions and the anticipated increase in domestic electricity demand.

Results of Capacity Market Main Auction

The fifth (FY 2024) auction targeted for the actual supply and demand of FY 2028

The contract price varies slightly depending on the region (area price). In the capacity market, contract prices are basically determined on a national basis, but there will inevitably be areas with a power shortage and areas with an excess. After that, fine adjustments are made continuously between areas with shortages and areas with surpluses, so that area prices are higher in areas with shortages and lower in areas with surpluses. The capacity market main auction is fundamentally treated as a single market nationwide (excluding Okinawa). However, market separation took place during the clearing process, resulting in significant differences in the contract price across areas.

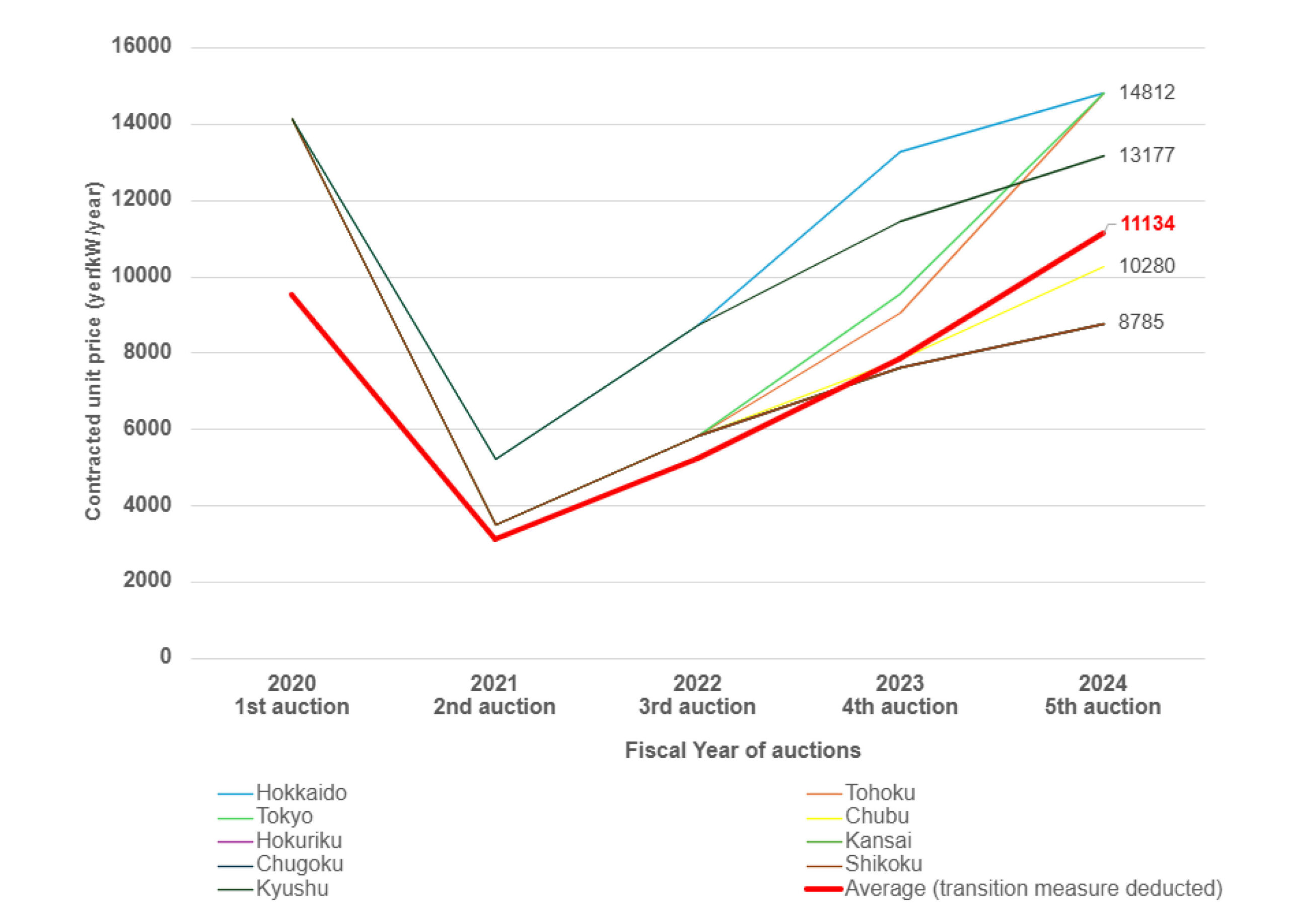

In this auction, the benchmark price (NetCONE) was set at 9,875 JPY/kW. Consequently, the area price exceeded the benchmark price in all areas except for the Hokuriku, Kansai, Chugoku, and Shikoku areas. The price in the Hokkaido, Tohoku, and Tokyo areas was 14,812 JPY/kW, hitting the upper price limit of this auction (1.5 times the benchmark price of 9,875 JPY/kW). Additionally, in the Kyushu area, market separation once again resulted in an area price determined as “1.5 times the area price of the adjacent area.” Any bids exceeding this threshold were set as the clearing price under the multi-price method.

| Total contracted capacity | 106.210,000 kW | |

| Area Prices | Hokkaido/Tohoku/Tokyo | 14,812 JPY/kW |

| Chubu | 10,280 JPY/kW | |

| Hokuriku/Kansai/Chugoku (Shikoku) | 8,785 JPY/kW | |

| Kyushu | 13,177 JPY/kW | |

| Total contracted amount based on transitional measures | 1.8506 trillion yen | |

Area Prices and average unit price in the Capacity Market Main Auction

Figure 1 Evolution of contract prices at the Capacity Market Main Auction

Source: Materials from the 99th meeting of the Working group for reviewing the scheme under the Electricity and Gas Basic Policy Subcommittee (February 5, 2025), compiled by RTS Corporation

Perspectives of considerations for future auctions

- In the fifth auction, the contract price was the highest since the 2nd auction across all areas, suggesting that the cost of maintaining and managing power sources participating in the capacity market auction has been increasing

- How should the results, where supply reliability was insufficient in Hokkaido, Tohoku, Tokyo, and Kyushu areas, be interpreted?

- In the capacity auctions of the UK and the US PJM, recent contract prices have surged. How should the status of Japan’s capacity market be assessed in light of these international trends?

- Similar to the 4th auction, the 5th auction also showed a high winning rate, and there is a forecast of increasing power demand from data centers, semiconductor factories, etc. How should the issue of securing supply capacity be considered?