In May 2023, the G7 Hiroshima Summit was held in Hiroshima, Japan and the Leaders’ Declaration covering a wide range of topics was issued. In the energy field, the joint communiqué issued at the G7 Ministers’ Meeting on Climate, Energy and Environment, held in April 2023 in Sapporo, was reflected in the Leaders’ Declaration, in which various pathways according to each country’s energy situation, industrial and social structures, and geographical conditions were acknowledged and it was decided to strengthen the efforts to holistically address energy security, the climate crisis, and geopolitical risks including the expansion of the global use of renewable energy toward the net zero carbon emissions by 2050.

As for renewable energy, it was specified that it is necessary to significantly accelerate the installation of renewable energy as well as the development and deployment of next-generation technologies and that the G7 member countries will contribute to expanding renewable energy globally and bring down costs by increasing the cumulative PV installed capacity to 1 TW or more (≥1TW) and collectively increasing offshore wind capacity by 150 GW, by 2030.

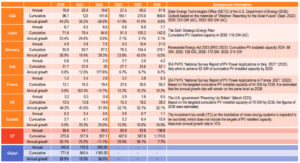

According to the IEA PVPS Snapshot Report, the global annual and cumulative PV installed capacities in 2022 were 240 GW and 1.2 TW, respectively. As for the annual installed capacity, China ranked first with 106 GW, followed by the USA with 18.6 GW, and India ranked third with 18.1 GW. As for the cumulative installed capacity, China also ranked first with 414.85 GW, followed by the USA with 141.6 GW and Japan with 84.9 GW. As for the total of all the G7 member countries, the annual installed capacity was 39.2 GW, accounting for 16.3% of the global total, and the cumulative installed capacity was 357.1 GW, accounting for 30.1% of the global total. Installation of ≥1 TW level installed capacity by 2030, which means installing a capacity equivalent to the current global cumulative installed capacity, requires the G7 member countries to triple the current annual installed capacity to the 100 GW level by 2030.

As shown in Table 1, the PV installed capacity in 2030 is assumed to reach 1,175 GW from the calculations based on the actual PV installed capacities in 2022 and the installation targets and future policy developments of each of the G7 member countries, but its achievement will not be easy, and each of the G7 countries will be required to implement measures for further expansion of PV introduction.

Among the G7 member countries, four countries, namely the USA, Germany, Japan, and Italy, have already set their installation targets for 2030, whereas France has set its installation target for 2028, and the UK for 2035. Whilst there are countries planning to install ≥100 GW by 2030, i.e. the USA 550 GWAC (= 660 GWDC), Germany 215 GWDC, and Japan 118 GWAC (= 142 GWDC), the plans for Italy, France, the UK, and Canada aim at the 50 GW level at the maximum, so realization of the ≥1 TW installation as G7 member countries will be led by the USA, Germany, and Japan. In particular, the USA, whose installed capacity accounts for 56.2% of the total, holds the key.

In line with the acceleration of PV installation, the USA will vigorously push forward the expanded utilization of PV under the Inflation Reduction Act (IRA) and the Defense Production Act (DPA), as there is a need to simultaneously promote stable procurement of solar cells by expanding domestic production and to develop dispatchable power sources such as storage batteries. However, further support measures and legislations will become necessary to exceed 500 GW. Germany has completely withdrawn from nuclear power and is promoting expanded installation of renewable energy. PV Strategy was formulated in May 2023 to achieve the 2030 installation target of 215 GW, which was set forth in the Revised Renewable Energy Act. The Strategy specifies biennial installation targets in and after 2024 until 2030, and action plans for their realization, such as expanding introduction of ground-mounted PV systems, promoting rooftop PV system installations, speeding up of network connections, enhancing the acceptance of PV power generation, utilizing the tax systems, securing domestic and EU-regional supply chains, developing advanced technologies, are given as pathways to stabilize the annual installed capacity at the 22 GW level from 2026 onwards.

On the other hand, currently in Japan, expansion of installation is being promoted based on the energy policy of the Ministry of Economy, Trade and Industry (METI) and the environmental policy of the Ministry of the Environment (MoE), but from now onward, it will be promoted under the Basic Policy for the Realization of GX (Green Transformation) including energy security. To accelerate the departure from fossil fuels and the response to energy security toward realization of clean energy economics as a G7 member country, installation of renewable energy will be accelerated and when considering the short period of until 2030, the main axis will be on the PV installation. Movements toward conversion of power sources to renewable energy sources, mainly PV, are also gaining momentum from the power consumer side. Japan, like the USA and Germany, need to rethink its national strategy looking ahead to 2030 and beyond, to also focus on the energy security, in expanding PV installation and strengthening the PV industry. Japan is obliged to achieve its installation target for 2030 with certainty and to contribute to the G7’s goal of “≥1 TW PV installation by 2030”.

*1: Overpanelling ratio of Japan and the USA is assumed to be AC:DC = 1:1.2

*2: Actual data of 2020 and 2021 (except the UK) from IEA PVPS “Trends in Photovoltaic Applications 2022”

*3: Actual data of 2022 (except the UK) from IEA PVPS “Snapshot of Global PV Markets 2023”

*4: The UK’s installed capacity from the International Renewable Energy Agency (IRENA) “Renewable Capacity Statistics 2023”