With the enactment of the Acts for Establishing Resilient and Sustainable Electricity Supply Systems in FY 2022, the dissemination environment of PV power generation shifted from a phase based on the former FIT program to a phase based on the new FIT/FIP programs. It was announced that the PV installed capacity (the commissioned capacity) under the new environment amounted to 2,653,054 projects with a total capacity of 65.1GWAC, exceeding 2.5 million projects in total.

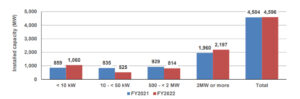

The annual PV installed capacity remained almost the same at 4,596 MWAC, with a slight increase from 4,584 MWAC in FY 2021 (the lowest annual PV installed capacity since FY 2013). As the newly approved capacity of PV projects was at a low level, the PV installed capacity in FY 2022 is supported by the start of operation of the PV projects which were approved under the former FIT program.

Compared to the PV installed capacity in FY 2021 by output capacity, the installed capacity of residential and other < 10 kW PV systems increased from 859 MW to 1,060 MW, and ≥ 2,000 kW extra-high voltage projects increased from 1,960 MW to 2,197 MW. Specifically, < 10 kW PV systems reached a level of 1 GW again, for the first time since 2013, showing an increasing trend. On the other hand, the installed capacity of low-voltage projects decreased from 835 MW to 525 MW, and 50 kW to < 2,000 kW high voltage projects decreased from 1,763 MW to 1,628 MW.

In FY 2022, while the approval cancellation of PV projects with a scale of 4 GW was observed, an increasing number of PV projects approved under the former FIT program which have not started operation for a long time started operation, and thus the capacity of these projects decreased to 9.0 GW as of the end of March 2023.

Figure 1 PV installed capacity in FY 2021 and FY 2022 based on the FIT/FIP programs

In or before 2020, the PV installed capacity based on the former FIT program was considered to be Japan’s PV installed capacity. Since 2021, however, PV introduction based on the budgets for PV dissemination (including supplementary budgets), which does not utilize the FIT program, by the Ministry of Economy, Trade and Industry (METI), the Ministry of the Environment (MoE), the Ministry of Land,Infrastructure, Transport and Tourism (MLIT), the Ministry of Agriculture, Forestry and Fisheries (MAFF), and each municipality as well as voluntary introduction making use of neither the FIT program nor dissemination budgets have started. As a result, with this additional introduction of 0.5 GWAC, Japan’s annual PV installed capacity in FY 2022 is expected to reach 5.1 GWAC.

Considering the facts that the recent capacity of newly approved PV projects has been sluggish and the capacity of the former-FIT-approved projects which have not started operation for a long time is decreasing, it is unclear whether Japan can maintain the annual PV installed capacity of 5 GWAC from now on. Since it has also become increasingly difficult to secure appropriate land for installing largescale ground-mounted PV systems, forming a new mixed-type PV market consisting of a wide range of segments such as houses, public and private facilities, ground-mounted PV systems, farmland utilization, and floating PV systems will be indispensable in order to achieve the target PV installed capacity for 2030. The prototype of this type of market has already been formulated under the former FIT program, and how we develop this from now on without imposing public burden will be an essential key to achieving the abovementioned target.

Toward achieving the target PV installed capacity for 2030, the capacity to be installed by the related government ministries and agencies have already been set. However, from the viewpoint of the PV industry and electricity consumers, etc. who actually work on PV introduction, setting the target PV installed capacity by market is also needed. Since it is expected that these markets will continuously develop and expand as important basic markets in and after 2030, setting the target PV installed capacity by market will help enhance predictability for forming a new PV market, and strengthen business foundations toward developing the PV industry including the creation of new players and businesses. Meanwhile, electricity consumers are expected to accelerate their efforts on PV introduction. Moreover, municipalities taking responsible roles in PV introduction can seek the expansion of PV introduction in local communities utilizing these markets toward revitalizing the local production and local consumption of energy as well as regional economy. What is required for the PV industry, which is now taking charge of Green Transformation (GX), is to achieve an independent and fullfledged growth based on the formation of a new PV market, focusing on the years after 2030 as well and also promoting the visualization of the PV market against the target PV installed capacity for 2030.

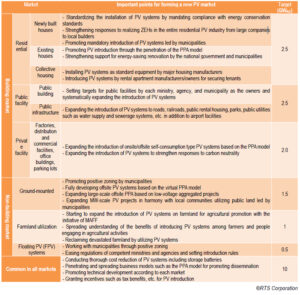

Table 1 Ideas on forming a new PV market for 2030 Market