Following the last month’s issue, this month we present our forecasts of the annual PV installed capacity in Japan for FY 2030 and FY 2035 by market segment.

The dissemination environment surrounding the PV market in Japan has been changing significantly in many aspects such as follows; 1) soaring prices of conventional energy, 2) transition to the FIT/FIP programs, 3) establishment of new subsidies for new introduction schemes and revisions of laws and promotion of regulatory reforms toward dissemination by relevant ministries and agencies, 4) penetration of introduction through PPAs, 5) the beginning of voluntary introduction without support from programs and subsidies, 6) pursuit of the promotion of green transformation (GX) for the formation of a decarbonized society, 7) progress of the transition to renewable energy electricity by electricity consumers, etc. Under the new dissemination environment as such, the formation of well-balanced markets in both building and non-building sectors shown below is about to move forward, toward the expansion of self-sustaining introduction of PV power generation.

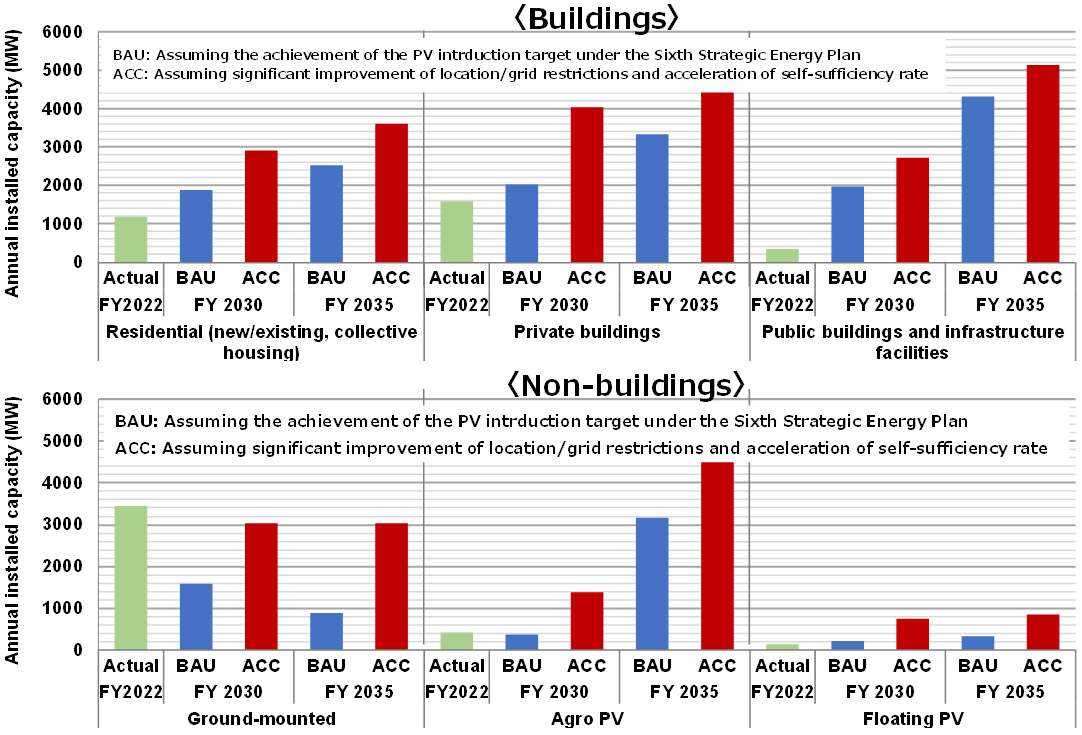

In the residential PV market, those who take charge of the installation works of the standard installation of PV systems are expanding from large-scale house makers to medium-scale ones and regional/local homebuilders. This is because of the rising electricity prices and preparations for disasters, etc. as well as the necessity to comply with energy-saving standards due to the revision of the Building Energy Efficiency Act. This trend is also strongly driven by the mandatory installation of PV systems on new houses stipulated by the municipalities such as Tokyo Metropolitan Government (TMG) and Kawasaki City of Kanagawa Prefecture.

In the private building market (factories, logistics facilities, commercial buildings and facilities, etc.), PV systems are increasingly becoming standard equipment, due to the expanding introduction of on-site PPA models and off-site PV power generation against the backdrop of rising electricity prices and strengthening measures to achieve carbon neutrality as well as the accelerating procurement of renewable energy electricity to comply with the Building Energy Efficiency Act and to enhance resilience.

In the public facility and infrastructure facility market, the initiatives to introduce PV power generation in public facilities based on the Government Action Plan will promote the introduction not only to the facilities of the governmental ministries and agencies but also to the public facilities owned by local governments nationwide. Furthermore, based on the Environmental Action Plan of the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), the introduction of PV power generation will be expanded not only to airports, but also to the entire infrastructure facility space such as roads, railroads, public rental housing, parks, etc.

While starting operation of the former FIT-approved projects until around 2025, the market of ground-mounted PV systems will newly shift to the MW-scale PV power plants in harmony with local communities and the municipal MW-scale PV power plants that utilize unused land and public land based on positive zoning by local governments. In addition, the off-site ground-mounted PV system installations utilizing unused land, vacant lots, parking lots, etc. will expand for bilateral transactions with consumers independent from the FIT/FIP programs.

In the market of PV systems on farmland, introduction will gradually expand with the establishment of the rules for PV on farmland (AgroPV) under the initiatives of the Ministry of Agriculture, Forestry and Fisheries (MAFF) based on the premise of sound development of agriculture. As a result, based on the successful cases that realized a well-balanced combination of farming and power generation as well as the cases of introducing PV power generation that regenerated abandoned farmland, facilitation of permission to convert agricultural land into the sites for PV installations and understanding of the merits of introducing PV power generation on farmland among farmers will begin to spread and then the introduction will begin to expand.

In the market of floating PV (FPV) systems, the introduction based on the past installation cases on reservoirs, agricultural water ponds, etc. will be promoted as well as the introduction through positive zoning in cooperation with local governments in charge.

Figure 1 shows the forecast of the PV market scale hereafter based on the outlook above, which assumes two cases; the business as usual (BAU) scenario which assumes the achievement of the installation target under the Sixth Strategic Energy Plan and the accelerated introduction (ACC) scenario which assumes the significant improvement in location and grid restrictions and the acceleration of the improvement of self-sufficiency rate.

The market for buildings, including houses, private facilities, public facilities, etc. will keep on expanding especially in the supply/demand integrated type until 2030.After that, with an aim to expand the introduction further toward FY 2035, in addition to the introduction of the systems to buildings, the introduction of the systems in the mixed-use non-building field is expected to expand, utilizing land that is already in use, such as roads, railroads, farmland, public land, etc. by fully using technological development, laws, systems and regulatory reforms, under the measures developed and implemented by the collective efforts of related ministries and agencies. Especially for Japan, which has location restrictions, it is important to show that farmland can be used for PV power generation without disturbing agriculture to promote carbon neutrality. By 2030, we need to have enough successful experience of realizing agriculture in harmony with power generation and to solve the issues about the introduction of PV power generation to arable farmland and to abandoned farmland, respectively. Furthermore, from 2030 onwards, it is necessary to evolve the current AgroPV into the one which contributes to the development of agriculture and to establish the AgroPV market that can simultaneously realizes food and energy security even when agriculture and power generation are integrated.