Japan’s Fiscal Year (FY) 2024 has ended, and FY 2025, starting on April 1, 2025, has begun. The biggest highlight of FY 2024 regarding PV power generation was the Cabinet’s approval of the Seventh Strategic Energy Plan (SEP), which positions PV as the top energy source in the FY 2040 energy mix, expected to supply 253 – 348 GWh of electricity (23 – 29% of total power generation). Until now, the PV deployment has been progressing toward the FY 2030 target of 120 GW. However, starting in FY 2025, it has entered a new phase, where the FY 2030 target is treated as a milestone, and efforts are focused on accelerating deployment toward 2040. In the Seventh SEP, PV is positioned as a distributed resource that supports self consumption and local production for local consumption of electricity, and the following approaches are presented: 1) Deployment premised on harmony with local communities and minimizing public burden; 2) Pursuing PV introduction where demand and supply are close to each other by making effective use of building rooftops and walls, and 3) Establishing a domestic supply chain for next-generation solar cells and industrial competitiveness.

With a focus on the global trend of expanding PV deployment, the plan aims to ensure a stable power supply from PV and develop the next-generation PV industry. The Seventh SEP identifies three pillars of future deployment as follows: 1) rooftop PV systems; 2) ground-mounted PV systems, and 3) the social implementation of next-generation solar cells. Relevant government ministries and agencies will promote policies focused on these three pillars. For rooftop PV systems, deployment will be categorized into the public sector, private facilities sector, and residential sector. For ground-mounted PV systems, designating efforts will renewable focus on energy promotional areas while targeting power generation projects that do not rely on the FIT or FIP programs, utilizing farmland, infrastructure spaces, and PPA/lease schemes. Furthermore, in the social implementation of next generation solar cells, efforts will focus on leveraging the lightweight and flexible characteristics of perovskite solar cells (PSCs) to explore new deployment areas, with a goal of achieving an installed capacity of 20 GW.

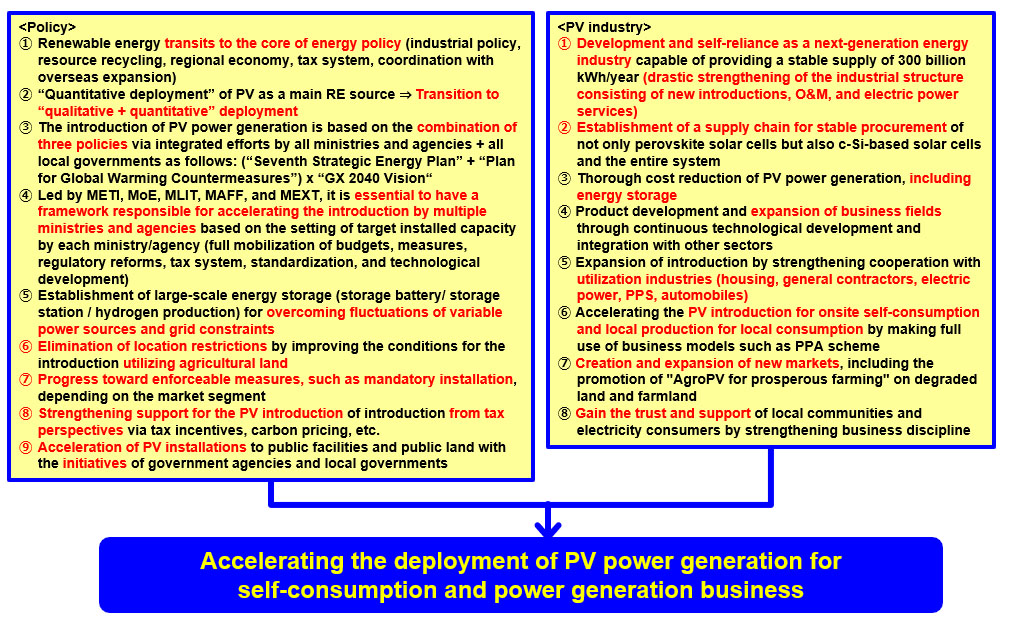

The aforementioned PV power generation of 253 – 348 GWh in FY 2040 corresponds to an installed capacity of 200-280 GW, based on the unit generation per capacity used in the Sixth SEP. Assuming that cumulative PV installed capacity up to FY 2024 is around 75 GW, additional 125 – 205 GW of new installations are needed by 2040. Under these circumstances, as shown in Figure 1, the future deployment of PV power envisioned in the Seventh SEP requires that renewable energy transition to the core of energy policy and be integrated with industrial policy, resource circulation policy, regional economic measures, tax systems, overseas expansion, and others. PV power generation has thus far focused on achieving “quantitative deployment” as a main renewable energy source, but moving forward, a shift towards “qualitative and quantitative deployment” will be required.

Since PV will also be deployed under initiatives such as the Plan for Global Warming Countermeasures and the GX 2040 Vision, which are integrated with the Seventh SEP, its advancement will be pursued through a concerted effort by all ministries, agencies, and local governments. Until now, the Ministry of Economy, Trade and Industry (METI) and the Ministry of the Environment (MoE), along with the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) and the Ministry of Agriculture, Forestry and Fisheries (MAFF), have played a central role in driving deployment through policy measures. Hereafter, it will likely be necessary to include the Ministry of Education, Culture, Sports, Science and Technology (MEXT), which is promoting initiatives for facilities making educational net-zero energy buildings (ZEBs). The expansion of deployment by the private sector is only possible with the drastic enhancement of a framework to accelerate deployment, through establishing deployment targets based on the policies administered by each ministry, and fully mobilizing measures by multiple ministries, budgets, legal frameworks, regulatory reforms, tax systems, standardization, and technological development. Furthermore, realizing this scale of deployment requires PV coupled with large-scale power storage (battery storage/hydrogen) and the utilization of farmland. Coupling with power storage can overcome the fluctuations of variable power sources and grid constraints, thereby enabling a stable power supply. As for farmland utilization, establishing installation conditions that prioritize agricultural activities will help resolve location constraints.

From the perspective of the PV industry, as it will be responsible for providing a stable supply of around 300 GWh/year of PV power, it must evolve beyond the current industrial model that primarily focuses on new installations. Instead, it needs to develop into a next-generation energy industry with an industrial structure that expands its business scope to include O&M and power services. On the other hand, the PV industry must establish a supply chain for stable procurement across the entire system—not only for perovskite solar cells (PSCs) but also for crystalline silicon (c-Si)-based solar cells, inverters, storage batteries, mounting structures, and the like, while also driving a thorough cost reduction in PV power, including energy storage. For electricity consumers, it is essential to lead the acceleration of PV deployment for onsite self-consumption and local production for local consumption of PV power by leveraging business models such as PPA schemes that do not rely on the FIT or FIP programs. Furthermore, the creation and expansion of new markets, such as promoting “AgroPV for prosperous farming” on abandoned land and farmland, will also be an important pillar.

FY 2025 will mark the start of the “Deployment Phase 2” aimed at achieving the 2040 installation target. During this fiscal year, the public and private sectors should clearly outline specific measures and action plans to accelerate deployment in the sectors identified in the Seventh SEP.

©RTS Corporation

Figure 1 Future responses required for solar power generation under the Seventh Basic Energy Plan