The International Energy Agency’s Photovoltaic Power Systems Programme (IEA PVPS), which has been monitoring global trends in PV installations since the 1990s focusing mainly on technological development and demonstration, has released its preliminary report on PV installed capacity in 2024 titled “Snapshot of Global PV Market 2025”.

The report highlights the remarkable growth in PV deployment that began in the year of the Paris Agreement – an international framework to combat climate change, including expanding the introduction of renewable energy toward the realization of a decarbonized society. Global perceptions of PV power generation have undergone transformation, with a significant the Paris Agreement serving as a turning point. The era of PV power generation has shifted from an “era of aiming to become a main power source” to an “era of playing a role as a main power source.” The PV deployment has expanded from “being limited to a few specific countries” to “being adopted worldwide”, and PV power has grown into the least expensive energy source capable of contributing to energy security.

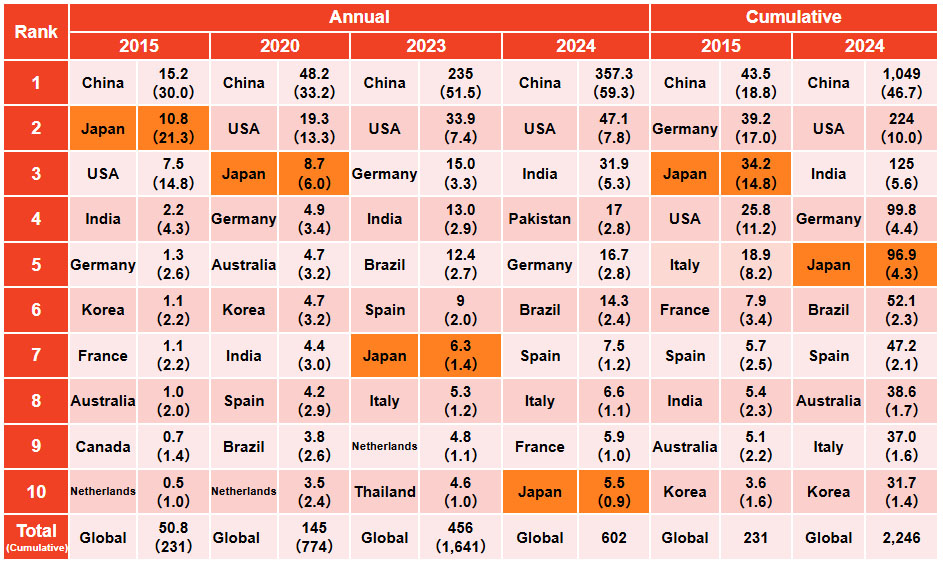

Looking at the progress over the decade from 2015 when the Paris Agreement was adopted through 2024 in terms of installed capacity, as shown in Table 1, the annual PV installed capacity increased from 50.8 GW to 602 GW, reaching an average annual growth rate of 31.6%. In 2024, the market surged past the 500 GW range, jumping from 456 GW in the previous year to the 600 GW scale. This rapid expansion was driven by the global spread of large scale PV installations, particularly MW solar projects, following the adoption of the Paris Agreement. At the same time, mass production of PV modules at the 10 GW scale became a reality, significantly enhancing PV power’s cost competitiveness against conventional power sources. As the global expansion of PV deployment became more foreseeable, competition intensified in capital investment to increase PV production capacity. This, combined with improvements in conversion efficiency reaching into the 20% range, led to further reductions in PV module prices. In the 2000s, as competition for higher performance and larger-sized PV cells/modules intensified, the demand side also began to evolve. PV introduction via public tenders and power purchase agreement (PPA) models emerged, further strengthening PV power’s economic advantage over conventional power sources. Moreover, the global surge in energy prices triggered by Russia’s invasion of Ukraine underscored the value of PV power as a quickly deployable solution for energy security. As a result, this recognition accelerated deployment, and the PV installed capacity in 2023 nearly doubled compared to the previous year.

As PV deployment continues to expand globally, China’s installed capacity stands out prominently. Under the leadership of the government, China has become the world’s largest producer of PV products and has also maintained its position as the top country in terms of installed capacity since 2013. Moreover, its global market share has increased year by year, surpassing 50% in 2023 onwards and approaching 60% in 2024. While Japan and Germany once held the second position, the United States has consistently maintained this position since 2020. In particular, PV deployment in the U.S. has surged since 2023, nearing an annual installed capacity of 50 GW. India ranks third, steadily promoting PV through energy and industrial policies, and has reached an annual market of 30 GW. Among emerging PV markets, Pakistan and Brazil rank fourth and sixth respectively, each achieving over 10 GW of annual installations. Germany, in fifth place, has chosen to phase out nuclear power and is actively pursuing decarbonization with renewable energy. With the national target of “215 GW of PV power by 2030” in place, the country implemented PV deployment initiatives based on the “PV Strategy (May 2023)” and the market has reversed the previous stagnation, leading to a sharp increase in installations, which have rapidly grown to 16.7 GW. Countries like Italy, Spain, and France, which were once key players alongside Germany in driving PV deployment, have also resumed to increase PV installations. Although their annual installations remain below 10 GW, they have started to grow again and have now surpassed Japan.

The global cumulative PV installed capacity reached 1 TW in 2022, up from 231 GW in 2015, and further increased to 2.2 TW in 2024. In terms of cumulative installations, the top five countries are China, the United States, Germany, and Japan, each with steady deployment, along with India, which has rapidly accelerated its expansion to become the world’s third-largest PV market. China, which ranks first in cumulative PV installed capacity as well, held an 18.8% share in 2015, with only a small gap separating it from Germany and Japan. However, by 2024, China became the first country to surpass 1 TW in cumulative PV installed capacity, approaching a 50% global share. The United States reached the 100 GW milestone in 2021, followed by India in 2024. Germany and Japan are both nearing the 100 GW mark as well.

In Japan, PV deployment surged following the introduction of the Feed-in Tariff (FIT) program, but after peaking at 10.8 GW in 2015, it has entered a downward trend, declining to 5.5 GW in 2024. While the global market entered an upward trajectory following the 2015 Paris Agreement, Japan has moved in the opposite direction. In 2015, Japan was the world’s second largest annual PV market, but in 2020 it fell to third place, and since then its ranking has declined rapidly, dropping to tenth place in 2024. In terms of cumulative installations, Japan has maintained fifth place thanks to years of steady deployment, but it is now being closely pursued by countries ranked sixth and below. As of 2024, there remains a gap of over 40 GW, so it is unlikely that Japan will be overtaken by the followers within the next year or two. However, both the public and private sectors must promptly expand PV deployment based on the Seventh Strategic Energy Plan, and, like Germany, pave the way for a return to large-scale deployment, aiming to achieve annual installations on the scale of 10 GW.

Table 1 Global Top 10 PV markets (annual and cumulative)

©RTS Corporation