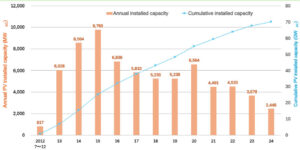

The PV installed capacity under the Feed-in Tariff (FIT) and Feed-in Premium (FIP) as of the end of December 2024 has been published, as shown in Figure 1.

The FIT program took effect in July 2012, and from April 2022, it transitioned to a combination of the FIT and FIP programs. The cumulative PV installed capacity under the two programs has reached 70.0 GWAC (with 5.6 GWAC having been installed prior to the start of the FIT program). Since the approved capacity is 75.1 GWAC, the remaining capacity yet to be brought online under these programs is 5.1 GWAC at the maximum. The majority of installations over the five-year period from 2020 to 2024 were based on PV projects approved in the 2010s. Due to the sluggish pace of new approvals during this period, the capacity of approved projects coming online has declined year by year, resulting in a sharp drop in annual installed capacity – from 6.6 GWAC in 2020 to 2.4 GWAC in 2024.

As such, PV deployment under the FIT and FIP programs has been on a declining trend. Meanwhile, since the adoption of the Sixth Strategic Energy Plan in October 2021 – which aimed to establish a decarbonized society – installations supported by renewable energy budgets through policy measures overseen by relevant ministries, namely, the Ministry of Economy, Trade and Industry (METI); the Ministry of the Environment (MoE); the Ministry of Land, Infrastructure, Transport and Tourism (MLIT); and the Ministry of Agriculture, Forestry and Fisheries (MAFF)) have been expanding. In addition, installations through mechanisms such as PPAs that do not rely on the FIT/FIP programs or subsidies have also begun to increase, driven by a growing number of electricity consumers shifting toward green power.

©RTS Corporation

Figure 1 Annual PV installed capacity under the FIT and FIP programs

Source: Website related to the Act on Special Measures Concerning Procurement of Electricity from Renewable Energy Sources by Electricity Utilities (Renewable Energy Act), compiled by RTS Corporation

The target PV deployment installed capacity for 2040, as outlined in the Seventh Strategic Energy Plan, calls for installations over the next 15 years that is double the installed capacity to date. To meet this target, annual installed capacity must be increased from the current level of around 5 GWAC to a range of 10 – 20 GWAC. Achieving this scale will require overcoming location restrictions and grid constraints, while steadily securing suitable locations and dispatchable power sources. At the same time, it is essential to develop the building segment – comprising public facilities, commercial buildings, and residences – and the non-building segment – comprising ground-mounted systems, use of agricultural land, and floating PV (FPV) – into self-sustaining markets. This must be accompanied by the reestablishment of the PV industry, which will play a central role in leading this transition.

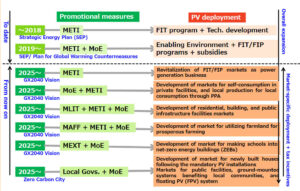

In the last month article in this section, we, RTS Corporation, presented estimated PV installed capacity by market segment based on the target PV installed capacity outlined in the Seventh Strategic Energy Plan. In order to guide the various market segments – each with differing business environments in terms of players, business models, users, and legal frameworks – toward self-sufficiency and growth, it is also necessary to implement market-specific policy measures, as illustrated in Figure 2. If relevant ministries can effectively coordinate and apply their respective policies according to the characteristics of each market, it may be possible to pave the way for market development that supports full-scale adoption and autonomous deployment. Unlike other renewable energy sources, PV is a power source that electricity consumers themselves can install. Therefore, it is no exaggeration to say that the promotion and acceleration of autonomous adoption by electricity consumers will be a key factor in determining PV installed capacity hereafter.

Accordingly, while continuing to support installations through existing schemes and subsidies for power generation businesses, it is also essential to implement policy measures, regulatory reforms, and legal frameworks that encourage voluntary adoption by electricity consumers, enabling them to treat PV as an essential part of daily life or business operations. In addition, a fundamental strengthening of the PV industry – one that is built on trust and accountability—is also necessary to support this transition.

©RTS Corporation

Figure 2 Promotional measures to revitalize the PV market toward the expansion of PV deployment