In February 2025, the GX 2040 Vision, the Seventh Strategic Energy Plan, and the Plan for Global Warming Countermeasures were simultaneously approved by the Cabinet, setting out national policies and goals for the government to comprehensively promote stable supply of energy, economic growth, and decarbonization with all-out effort.

This has begun to show signs of renewed expansion in PV deployment, which had stagnated since FY 2021. The Ministry of Economy, Trade and Industry (METI), taking initiative in expanding PV deployment, the Ministry of the Environment (MoE), the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), and the Ministry of Agriculture, Forestry and Fisheries (MAFF) are, individually and in collaboration, leveraging their respective policies, budgets, legal frameworks, regulatory reforms, technological development, and tax measures to promote the PV deployment in six key markets: public facilities, private facilities, residential, ground-mounted, Agro PV, and floating PV installations.

Local governments, in collaboration with MoE, are promoting PV deployment to establish regions that encourage renewable energy adoption and to achieve zero-carbon cities. The PV industry, working together with conventional energy industries, utilization industries, and the financial sector, is advancing deployment toward self-sufficiency through both power generation projects using the FIT and FIP programs and self-consumption projects under the PPA model. Meanwhile, the national and local governments, private companies, and individuals – as electricity consumers – recognize the importance of efforts toward a decarbonized society and have begun transitioning to green power. Moving forward, in addition to strengthening these ambitious initiatives on the administrative and supply sides, it will be essential to accelerate PV deployment led by electricity consumers themselves.

The 2040 PV deployment target under the Seventh Strategic Energy Plan corresponds to 200 – 280 GWAC of generation capacity. Since the PV installed capacity at the end of FY 2024 (end of March 2025) is around 75 GWAC, an additional 125 – 205 GWAC of new installations will be required over the next 16 years. A realistic approach to achieving this target would be to steadily expand PV deployment while developing and expanding the market, aiming for 10 GW by 2030, 15 GW by 2035, and 20 GW by 2040. Since the cumulative deployment target for perovskite solar cells (PSCs) by 2040 has already been set at 20 GW, the majority of future installations will continue to be based on crystalline silicon (c-Si) technology as is currently the case. Including additional PV capacity to replace decommissioned systems and for repowering, the required PV capacity will increase further.

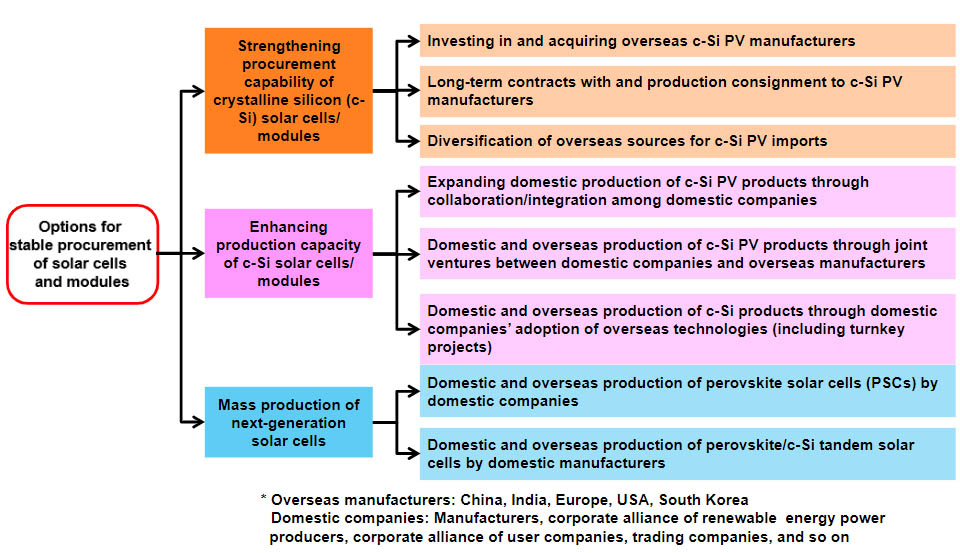

Currently, more than 90% of the PV installed capacity in Japan depend on overseas sources, mainly imports from China. Presently, efforts to establish a domestic supply chain for next-generation solar cells are focusing on the production of PSCs. However, in order to substantially expand PV power generation as a mainstream, primary power source, it may be time to also consider a strategy for ensuring the stable procurement of c-Si solar cells. The supply-demand situation for solar cells has recently been characterized by a global oversupply, allowing for inexpensive procurement despite the weak yen. However, in China, corrective measures to address overproduction are beginning to emerge. Meanwhile, globally, against the backdrop of expanding the annual PV market to the TW (terawatt) scale and its recognition as the world’s lowest-cost power source, PV production facilities are being established in demand regions such as the United States, Europe, India, and Southeast Asia, leading to a restructuring of the supply chain. In Japan as well, domestic production of both PSCs and c-Si solar cells should be considered.

As illustrated in Figure 1, the public and private sectors should collaboratively examine approaches to ensure the stable, medium- to long-term procurement of solar cells. PV power systems are composed not only of PV modules but also of other key equipment such as inverters and storage batteries, so it is necessary to consider stable procurement for the entire PV system. Recently, Mitsubishi Corporation announced its withdrawal from the offshore wind power business, citing soaring procurement costs as the reason. This suggests that supply chain restructuring will also become increasingly important for PV power generation in the future.

In the next stage of development for c- Si solar cells, whose conversion efficiency is approaching its limit, a global race has begun to develop a c-Si/ perovskite tandem solar cell aiming for conversion efficiencies exceeding 30%. In addition to developing production technologies for PSCs, it will also be necessary to prepare for the era of ultrahigh- efficiency tandem solar cells achieved through the integration with c- Si solar cell production technologies.

©RTS Corporation

Figure 1 Options for stable procurement of PV modules in preparation for the annual PV installed capacity exceeding 10 GW in Japan