In the European Union (EU), PV power generation accounted for 22.1% of the total power generation in June 2025, becoming the largest power source for the first time ever. Due to the expansion of PV installations and continued sunny weather, with at least 13 of the EU member states recording their highest ever month of PV power generation. According to the International Energy Agency’s Photovoltaic Power Systems Program (IEA PVPS), the contribution of PV power to electricity demand at the end of 2024 was 28.9% in Spain and 21.3% in the Netherlands, and PV is already the main power source in some parts of Europe.

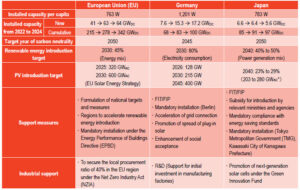

As of the end of 2024, the cumulative PV installed capacity in Europe reached 343 GWdc. The EU has set a cumulative installed capacity target of 600 GWac in 2030 in the EU Solar Energy Strategy formulated in March 2022.This target is equivalent to 740 GW in DC equivalent, so about 400 GW of new installations are required between 2025 and 2030 to achieve it. Member states are expected to promote the introduction of PV power generation in accordance with the National Energy and Climate Plan (NECP), which specifies efforts to achieve each target, and mandatory installation under the Energy Performance of Buildings Directive (EPBD) is planned to be implemented in phases. Following the introduction of variable power sources, electricity market reform is also essential. Meanwhile, the EU legislated electricity market reform in May 2024, aiming to create a more resilient and sustainable energy market by promoting long-term contracts for non-fossil energy, implementing cleaner and more flexible solutions, and improving market transparency.

In Germany, which leads the European market, there were concerns about a setback in policies addressing climate change due to a change of administration, but the target for the introduction of renewable energy and PV power generation by 2045 was maintained. Germany set a target for the cumulative PV installed capacity, under the PV Strategy formulated in May 2023 , at 215 GW by 2030 and 400 GW by 2040. To achieve this, measures such as expanding the bidding quota, and applying subsidies (bonuses) to PV systems for special locations, such as AgroPV systems, floating PV (FPV) systems, and those for wetlands and parking lots have been proposed. In February 2025, while the price guarantee by the Feed-in Tariff (FIT) program was abolished during periods when electricity prices are negative, preferential measures were also provided for smart meter installers and those who switched to the new scheme, and measures were launched to avoid overloading the power grid and ensure the safety of the energy system. In addition, it was decided to expand gasfired power as a dispatching capability in preparation for the expansion of variable power sources.

In addition to climate change countermeasures, the EU has also begun to work on the competitiveness of industries in the region due to the geopolitical situation. According to the Net Zero Industry Act (NZIA), 40% of the demand for products that contribute to net zero greenhouse gas emissions, such as pv modules, is required to be covered by products manufactured in the region, and the EU plans to strengthen efforts to ensure a stable supply of PV products and the security of power generation facilities.

In Europe, issues such as grid constraints, development of PV projects in harmony with local communities, and location constraints are becoming apparent, but various measures are expected to be implemented in the future to achieve the ambitious goal of introducing PV power generation.

In Japan, the Seventh Strategic Energy Plan (SEP) was formulated in February 2025, and PV power generation is positioned as the top power source in terms of power generation capacity and power generation amount by 2040. However, Japan’s annual PV installed capacity in 2024 has decreased from the 6 GW level to the 5 GW level.

As shown in Table 1, the EU and Germany have not only formulated targets for the PV installed capacity, but also set out “strategies” that outline the measures, and have made great progress in expanding PV installations again. In particular, Germany, under the Solar Power Strategy,” plans to expand to the annual PV market to 22 GW by 2026, tripling from 2022, and maintain 22 GW thereafter. As a breakdown of 22 GW per year, the same capacity of groundmounted installations and rooftop installations is set at 11 GW. As a result, the annual installation has doubled from 7 GW to 15 GW, expanding to 17.2 GW in 2024.

For Japan, in order to achieve the 2040 target, the public and private sectors must work together to set and implement measures and processes to achieve the introduction targets set in the Seventh SEP for each market, and formulate a “self-reliance and development strategy” specialized in PV power generation in which both the supply and demand sides can invest 2 and expand their introduction. At the same time, in order to increase social acceptance, the PV industry must thoroughly pursue “business discipline and coexistence” in line with the policy for ensuring PV projects in harmony with local communities and strengthening discipline in the PV business, which is currently being discussed by the Interministerial liaison meeting.

Table 1 PV power generation in EU, Germany and Japan

*: Estimates by RTS Corporation

©RTS Corporation