Year 2026 has begun, and the first year of expanding the PV installations has started, in line with the Package of Measures for MW-scale PV Projects, in addition to the Seventh Strategic Energy Plan. Fourteen years have passed since the initial FIT program started in 2012, and the cost of PV power generation has declined to a level that can compete with conventional power sources. Accordingly, FY 2026 starting in April 2026 will be the final year for commercial ground-mounted PV systems (10 kW or more), to be supported by the FIT and FIP programs, and they are expected to be excluded from the scope of the two programs from FY 2027 onwards.

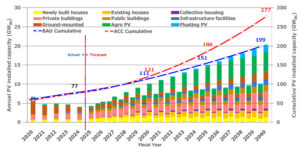

Under these circumstances, we, RTS Corporation made a forecast on the PV installed capacity by market based on the Seventh Strategic Energy Plan, as shown in Figure 1. There are two scenarios for the forecast: the BAU (business as usual) scenario and the Accelerated scenario. The former scenario assumes the realization of the lower limit 23%, and the latter scenario assumes the realization of the upper limit 29% of the ratio of PV power generation in the FY 2040 energy mix indicated in the plan.

From the two scenarios, the cumulative PV installed capacity in Japan is forecasted to be 111 to 121 GWAC by FY 2030, 151 to 186 GWAC by FY 2035, and 199 to 277 GWAC by FY 2040, whereas the annual installed capacity is forecasted to grow from 7.1 to 10.1 GWAC by FY 2030, to 8.6 to 15.1 GWAC by FY 2035, and to 10.2 to 20.3 GWAC by FY 2040 (on a PV system capacity basis).

Considering the current situation and new markets that are expected to grow in the future, the forecast was made for the following six markets: 1) residential (detached houses); 2) private buildings; 3) public and infrastructure facilities; 4) ground-mounted PV systems; 5) agrivoltaics (Agro PV) and 6) floating PV systems.

In the residential PV market, newly built detached houses are increasingly required to comply with energy-saving standards under the Building Energy Conservation Act and energy-saving standards are being raised, and the installation of PV systems as standard equipment not only by major companies but also by medium-sized house manufacturers and construction companies will become widespread. For existing houses, in addition to strengthening support for the PV introduction on existing detached houses by local governments, etc., the introduction with the support of the FIT and FIP programs for initial investment and the penetration of the PPA scheme will expand, and retrofit PV installations will be made to existing houses. In the case of collective housing, the installation of PV systems as standard equipment by major condominium developers is expected to expand.

In the private building market, the PV introduction is expected to spread to factories and other facilities based on the Energy Conservation Act to promote the transition to green electricity, as well as the advantages of long-term fixed electricity costs and no upfront cost thanks to aforementioned initial investment support and PPAs. Furthermore, the PV introduction will grow to support net-zero energy buildings (ZEB), to enhance corporate value, and to respond to the request from the supply chain.

In the public buildings and infrastructure facilities market, the PV introduction to the facilities of all ministries and agencies and the buildings owned by local governments will expand as the initiative to introduce based on the “government plan” is progressing systematically. In addition to airports, the PV introduction to roads, railways, ports, parks and other infrastructure facilities is estimated to grow as well.

In the ground-mounted PV market, the introduction of MW-scale PV systems developed in harmony with local communities will be promoted by the establishment of renewable energy promotion areas by local governments, and desirable large-scale PV projects that are environmentally friendly will continue to be developed in harmony with local communities under the Package of Measures for MW-scale PV Projects. These PV systems will be introduced by off-site PPA and virtual PPA by private companies as well.

In the Agro PV market, the Ministry of Agriculture, Forestry and Fisheries (MAFF) has led the clarification of the definition of “desirable Agro PV power generation” and MAFF is expected to promote the expansion of its introduction through nationwide model projects, and the introduction of Agro PV systems for promoting agriculture will gradually expand. In the future, Agro PV is expected to be positioned as an important equipment that contributes to agriculture, and the understanding of the benefits of PV deployment will spread among farmers and agricultural stakeholders, and full-scale introduction will proceed.

Building on the previous installations, the floating PV systems will be introduced to agricultural reservoirs nationwide. Through demonstration tests, its introduction will also spread in relatively calm waters such as inland seas and bays.

Given these predictions, the annual PV installed capacity in Japan will be driven by the building market for housing and private buildings in close proximity to supply and demand until FY 2035, and from FY 2030 onwards, the Agro PV and the ground-mounted PV systems will also begin to grow again due to the steady establishment of development in harmony with local communities, and from FY2035 onwards, the building market and the non-building market will form both wheels of expansion of introduction.

However, since there is a limit to the expansion of PV deployment by economic feasibility and measures and regulatory reforms by national and local governments, this forecast assumed the expansion of the environment for deployment, including the PV industry, new markets, business models, overcoming constraints, and changes and developments in the social environment. The absence of any single element would create a bottleneck and hinder broader deployment.

The year 2026 must be a year in which all relevant parties, including the national and local governments promoting measures to expand PV deployment, the PV industry and user industries responsible for the stable supply and technological innovation of PV systems, and the electricity consumers who are accelerating the transition to green electricity, must unite to increase the deployment and transform the expansion of introduction from the stage of stagnation to acceleration.

@RTS Corporation

Note: BAU: “Business as Usual” scenario, ACC: “Accelerated” scenario

Figure 1 Forecasts of PV installed capacity in Japan from FY 2025 to FY 2040 (AC-based)