RTS Corporation released “The Current Status and the Outlook of the Residential PV Market in Japan (2020 Edition) -toward the Future Business Development” (Japanese report)

RTS Corporation released a special research report titled “The Current Status and the Outlook of the Residential PV Market in Japan (2020 Edition) -toward the Future Business Development” (Japanese report) on March 9, 2020.

The Japanese residential PV market is one of largest markets in the world, and sales distribution networks and product lineups are being enhanced. Over the last few years, the residential PV market has experienced downward trends and an adjustment period continued due to the rapid expansion of industrial PV systems based on the FIT program.

However, in 2019, the “post-FIT” PV systems started to appear ahead of the industrial sector and the business competitions over residential PV systems are intensifying once again, including storage battery systems. Together with the development of net zero energy houses (ZEH) and an increasing demand for resilience, the residential PV market in Japan is expected to grow further. There is no doubt that the residential PV systems will contribute to the infrastructure of local communities as distributed energy systems both for newly-built and existing houses, driven by the new business models such as Zero Yen installation (PV system installation at not initial cost) and proposals of PV systems for self-consumption.

The industrial PV systems are now reaching the turning point to seek for the “post-FIT” market. Under such circumstances, the residential PV market has been reassessed as the market where Japan’s industrial strengths such as high quality manufacturing and detailed services can be demonstrated, and a large number of businesses including those out of the PV industry are enhancing their efforts in entering into or expanding the residential PV business. Against these backgrounds, we, RTS Corporation made a forecast on the residential PV market in Japan based on two scenarios, BAU scenario and accelerated scenario (scenario based on accelerated installation and technology development) in the new report.

In addition to various statistics based on the fixed point observation, we compiled the outlook on the following as well, which will be helpful for strategically deploying the residential PV business toward the future: 1) distribution of residential PV systems; 2) measures for the “post-FIT” PV systems (system owners) and a forecast of the storage system market; 3) the next-generation business models including residential PV systems and 4) trends of the next-generation production related to the residential PV systems.

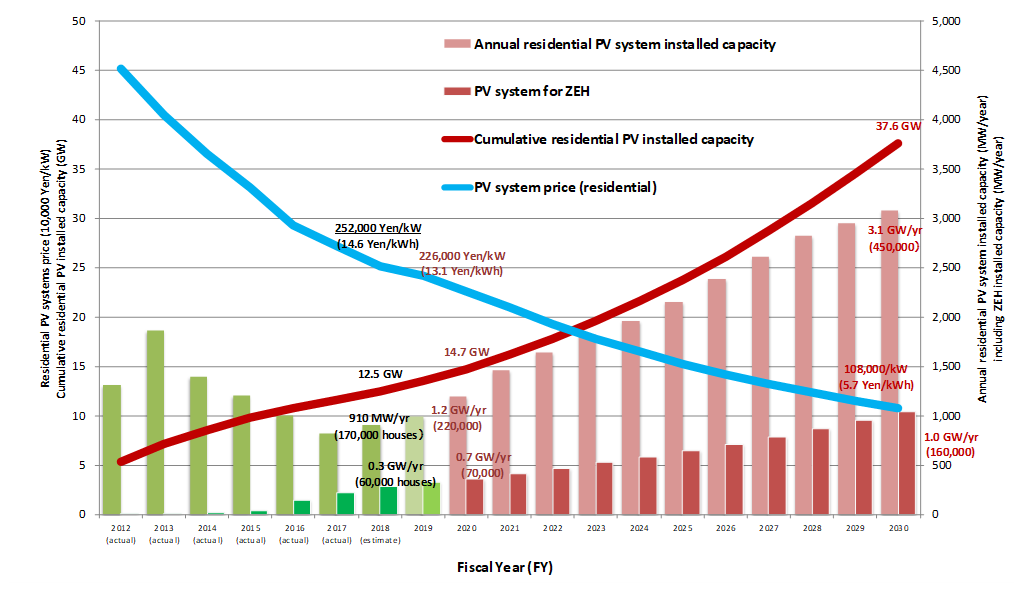

In Figure 1, “The roadmap of the residential PV market in Japan by RTS,” RTS forecasts that the residential PV system price will decrease from 252,000 Yen/kW ($ 2,330 /kW) at the end of FY 2018 ended March 2019 to 108,000 Yen/kW ($ 999 /kW) by the end of FY 2030 ending March 2031, a decrease of over 40 % under the accelerated scenario). As for the power generation cost (LCOE), we also forecast a significant reduction from the current 14.6 Yen/kWh (13.5 cents/kWh) to 5.7 Yen/kWh (5.27 cents/kWh) by the end of FY 2030. This means that the cost target of the Japanese government “7 Yen/kWh (6.47 cents/kWh) in 2030” will likely be achieved ahead of schedule.

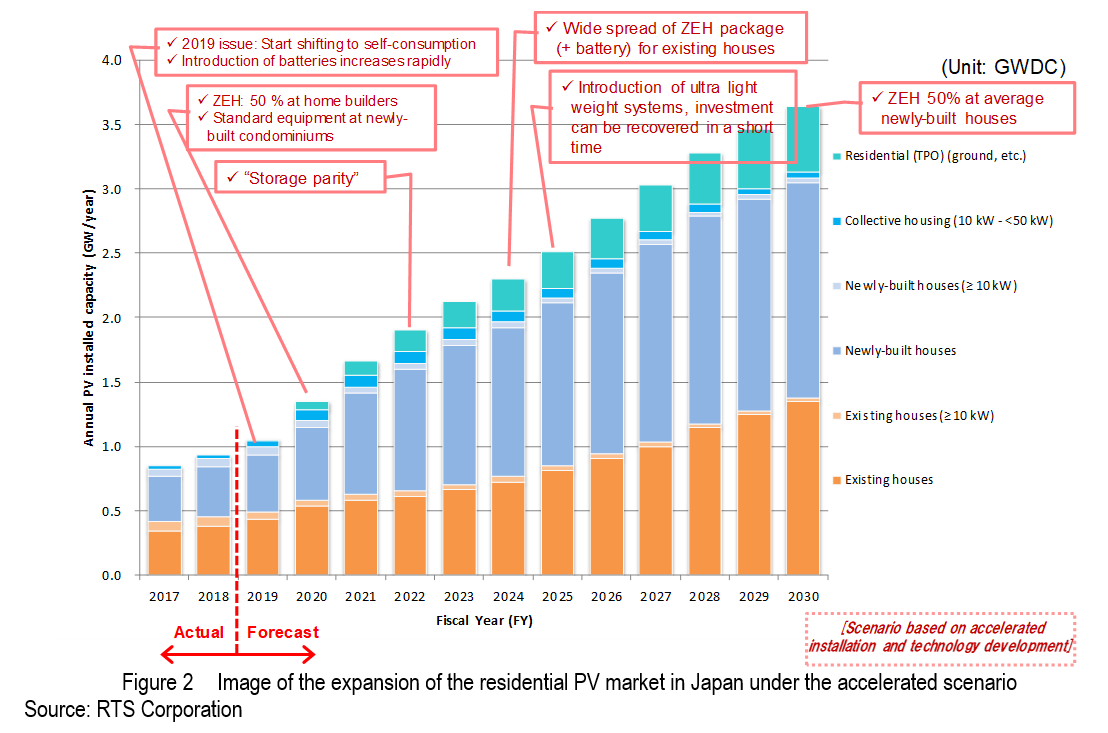

The residential PV market, which had been in the adjustment phase, is expected to recover hereafter, driven by the trend that both distributors and users will focus on PV systems for self-consumption, increase in PV installations in newly-built houses as standard equipment, as well as gradual expansion of ZEH installations. The residential PV market is expected to grow to the 2-GW/year level in the mid-2020s, and to 3.1 GW/year (cumulative: 38GW) by FY 2030. Also, while the obligation for newly-built houses to conform to the energy conservation standards under the Building Energy Efficiency Act has been postponed, actions to achieve zero energy, which is beyond energy conservation, will be accelerated with the residential top-runner program and advanced efforts by ZEH builders and planners as the driving force. We forecast that the ZEH market, mainly based on the newly-built houses, will increase from the current level of 60,000 houses to 160,000 houses by FY 2030, accounting for over 50 % of the entire newly-built housing market (280,000 houses), which will likely achieve the roadmap drawn by the national government.

It is expected that the residential PV market in Japan will shift to the recovering and expanding trends, driven by the increasing shifting to PV systems for self-consumption, the expansion of TPO/ PPA businesses symbolized by the Zero Yen installation model (so-called the “roof-leasing” business), dissemination of smart products for the post-FIT users and other leading users following the year 2019 issue and so on.

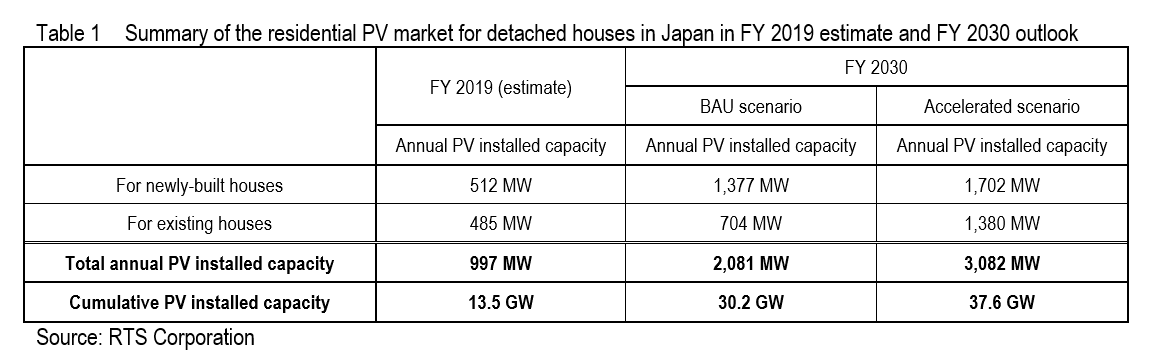

In the 2020s, it is estimated that the PV systems for newly-built houses will be disseminated ahead of other applications. However, under the BAU scenario, it is expected to hit the ceiling by 2030, and the annual market size will be 2.1 GW (310,000 houses) in FY 2030 including the PV systems for both newly-built and existing houses. Under the accelerated scenario, the market will continue growing in the 2020s and reach the annual market size of 3.1 GW (450,000 houses) in FY 2030, driven by the improvement of PV installation ratio for newly-built houses and the expansion of product lineups which can respond to the demand for existing houses through technology development.

In addition to those mentioned above, PV markets for collective housing (apartments and condominiums), non-rooftop PV systems exclusively for supplying electricity to houses (TPO models for ground-mounted PV systems, etc. are assumed) are also considered as the markets related to the residential PV market. By FY 2030, the entire residential PV-related market is likely to grow to 2.4 GW/year under the BAU scenario and 3.6 GW/year under the accelerated scenario.

Moreover, the following items have been sorted out as important points when considering the future market.

- The number of new housing starts will steadily decrease due to the expected decline in the population and the number of households. Assuming there are 630,000 houses in FY 2030, the number of newly-built detached houses is estimated to be around 280,000 among these 630,000 and the PV market for newly-built residential applications will be saturated.

- The number of existing houses will continue to increase, and the problem of the abandoned houses will be worsened. Along with the distribution and use of existing houses, measures such as energy conservation and securing of zero-energy performances, etc. and efforts to improve asset values through the “energy reform” will become important.

- Regarding the post-FIT business, a wide variety of new business models will emerge that have potential to increase the opportunities for introducing residential PV systems, including the following: Proposals of energy-creating, energy-storing and energy-conserving equipment to the post-FIT users (responses to heat demand as well), self-consumption systems which do not use the FIT, Zero Yen installation through TPO/ PPA models, collective purchase scheme (along with the cooperation by local governments), use of self-wheeling of off-site power generation, electricity-related business (regional PPS business, aggregation, demand response, VPP (virtual power plant), trading of CO2 emission reduction and environmental contribution values, electricity supply from third-party non-rooftop systems (use of TPO model), full-scale deployment of O&M business, integration with town development/ redevelopment projects, and so on.

- Development of the next-generation residential PV-related products based on the technology development is also expected: BIPV (roof materials, building materials, windows, etc.), high efficiency and high end products and small-sized AC modules for small roofs, ultra-light PV systems applicable to existing houses, which can recover investment in a short time, V2H (Vehicle to Home) systems for off-grid applications and improving resilience, environment-friendly power generation for IoT, PV-mounted electric vehicles (EV), and so on.

- Possibility of enhancing regulations to accelerate dissemination of residential PV systems: obligation to install (consider installation of) PV systems on newly-built buildings, voluntary environment-related targets and action plans in line with SDGs and ESG investment, and so on.

- Presentation of the concept of calculating the size of the “future-oriented market” including the value-added businesses related to residential PV systems such as O&M, storage systems, energy management and life-related services/

This report is written in Japanese. For details of this report, please access our Japanese Site.