The International Energy Agency (IEA) released a report on the developments of PV power generation in 2023 entitled “Trends in Photovoltaic Applications 2024”. The report comprehensively summarizes global PV trends, including market trends, policy trends, industrial trends, contributions to society and the environment, and price trends of PV power generation.

In 2023, 456 GW of PV was newly installed worldwide, bringing the total cumulative PV installations to 1.6 TW. This was nearly double the 242 GW installed in 2022, marking the highest growth in the past 10 years. New installations in 2024 are expected to reach around 600 GW, which would push the cumulative total to over 2 TW.

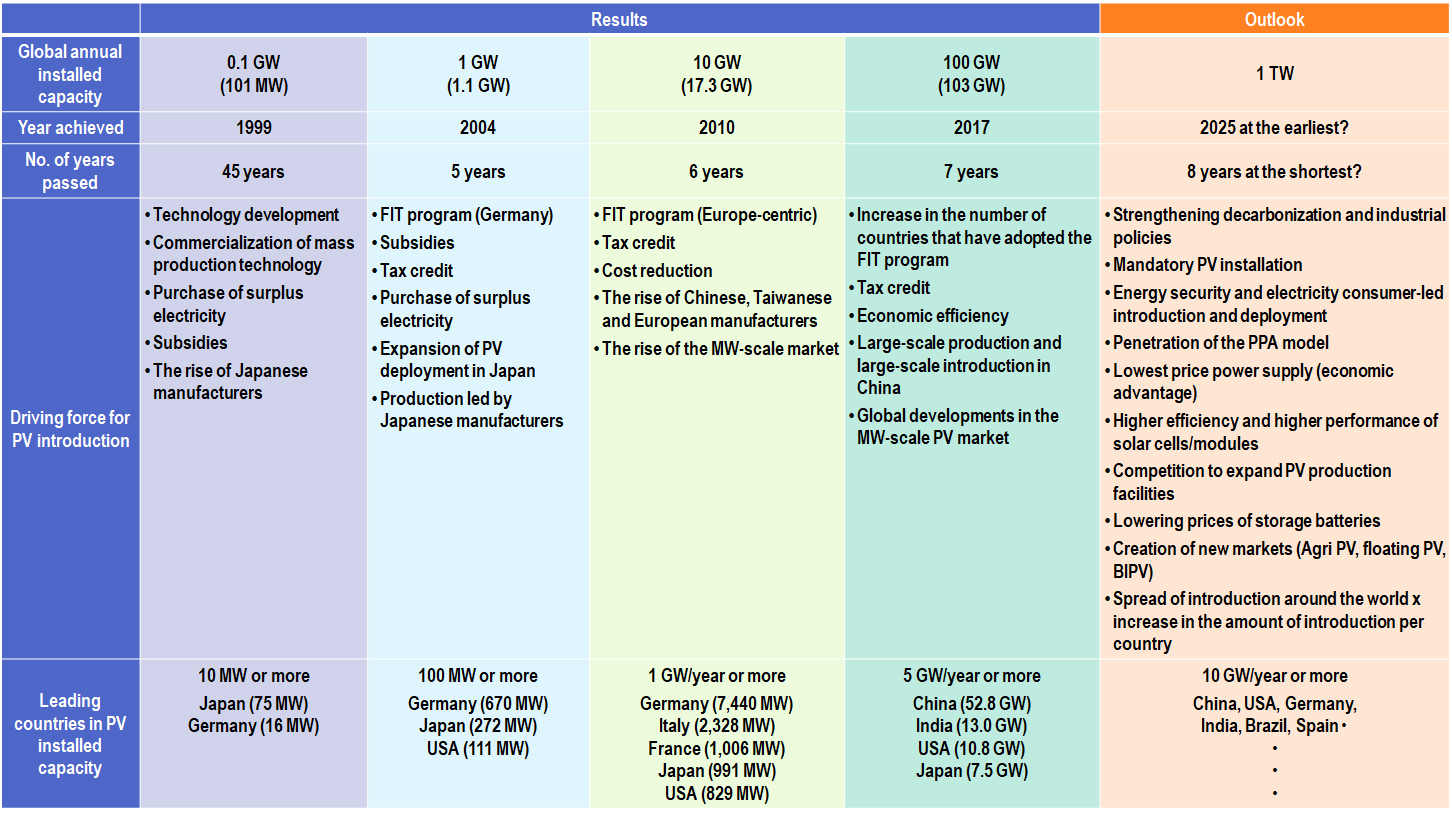

Looking back on the global annual PV installations since the milestone of 0.1 GW in 1999 as shown in Table 1, a driving force for the expansion of installations emerged over time, and the annual installed capacity evolved in stages, expanding to scales of 1 GW within 5 years by 2004, 10 GW within 6 years by 2010, and 100 GW within 7 years by 2017. Since the number of years it required for each 10-fold increase has increased by one year to go to the next 10-fold increase, the annual installations of 1 TW could be achieved by 2025, which is 8 years from 2017, at the earliest.

Figure 1 Driving force for the global expansion of PV installed capacity

It took 45 years from the invention of solar cells in 1954 to reach 0.1 GW of annual PV installed capacity. The experience of the first oil crisis in 1973 led to the initiation of the development of alternative energy sources to replace oil, primarily driven by Japan, the USA, and Europe, with PV power generation chosen as one of the alternatives. The development of technology regarding PV progressed to technology demonstrations and further developed into the development of initial market supported by subsidies. Japan’s subsidies specified for the installation of residential PV systems and surplus power purchases became a driving force for the global expansion of PV, growing to the annual PV installations of 0.1 GW level in 1999.

This was followed by Japan’s continued measures to expand residential PV systems, the USA’s promotion of PV introduction through tax credits, and furthermore, Germany’s establishment of the Feed-in Tariff (FIT) program along with an increase in the purchase price, all of which supported the introduction of PV, which was not yet economically viable, ultimately reaching 1 GW by 2004.

After that, adoption of the FIT program widely spread across Europe and the cost of PV decreased due to the start of low-cost solar cell supply by China and Taiwan, and in 2010, the annual PV installation entered the era of 10 GW. In the 2010s, China began mass production of solar cells and mass introduction of PV, and the power generation cost at large-scale PV power plants became as economical as conventional power sources. With the establishment of the Paris Agreement in 2015, the introduction of PV power generation, which was yet limited to a few specific countries, began to emerge globally such as India, and by 2017, the annual PV installations exceeded 100 GW. With the onset of the 100 GW annual installation era, countries around the world began to introduce PV as part of the decarbonization policies, mainly in the form of MW-scale PV power plants. As the predictability of the global expansion of PV installations increased, competition for capital investment to expand the supply capacity of solar cells intensified, and the price of solar cells also dropped more rapidly.

In the 2000s, solar cells began to become more efficient and larger in size, and business models for expanding introduction through tenders and PPAs began to spread, and PV power gained an economic advantage as the least expensive power source. Russia’s invasion of Ukraine triggered a sudden change in the energy situation and highlighted the importance of introducing PV from the perspective of energy security, and the world is moving toward an annual introduction of 1 TW. Meanwhile, due to the lowering price of storage batteries, PV power generation itself has also evolved into PV systems equipped with storage capabilities to reduce the strain on the grid, and the area of utilization of PV as a distributed power source expanded. Commercialization of new types of solar cells, such as perovskite solar cells (PSCs), will also make the expansion of the installation areas possible.

Under such situation, Japan’s annual PV installed capacity peaked at 10.8 GW in 2015 and has since declined, with steady installations at the 6 to 8 GW level. Recently, a downward trend could also be observed. Germany, which pioneered the FIT program, saw a decline in annual installations and stagnated after reaching a peak of 8.2 GW in 2012, but began recovering around the year 2020. By formulating a PV power generation strategy to achieve the 215 GW target for 2030 set in the Renewable Energy Act 2023, annual installations reached 15 GW in 2023, significantly surpassing its previous peak, marking a remarkable comeback. Introduction of PV in Japan started to progress through policy initiatives by relevant ministries and agencies, in addition to the FIT and FIP programs, and formation of a stable market with annual installations of 10 GW or more in both the building and nonbuilding markets is achievable. The current deliberations toward the formulation of the Seventh Strategic Energy Plan are at an important juncture, as it will determine the direction of the energy mix toward 2040 and indicate the national goal. The PV installation target to be set this time should fully incorporate the future growth potential of PV power generation and should strategically pursue a high goal that will contribute to the global expansion of the PV deployment. As PV power will continue to be a main power source leading the way toward carbon neutrality, this opportunity must be made the most use as a great chance.