In order to expand the use of perovskite solar cells (PSCs), the “Next-Generation Solar Cell Strategy” has been formulated, which aims to introduce 20 GW of next generation solar cells by 2040 (40 GW or more if a significant cost reduction is achieved). In contrast to crystalline silicon (c-Si) solar cells, which currently dominate the global PV market, PSCs, which can be installed in places where it had been difficult to install PV modules on rooftops, etc., are positioned as the next-generation solar cell that can be used to broaden the applications by taking advantage of their lightweight and flexible features.

In May 2024, the Ministry of Economy, Trade and Industry (METI) established the “Public-Private Council for Expanding the Introduction of Next-Generation Solar Cells and Strengthening Industrial Competitiveness” that consists of academic experts, supply side, user side, and government related ministries and agency (METI/ Ministry of Land, Infrastructure, Transport and Tourism (MLIT)/ Ministry of the Environment (MoE)/ Ministry of Defense (MoD)/ Ministry of Education, Culture, Sports, Science and Technology (MEXT)/ Ministry of Agriculture, Forestry and Fisheries (MAFF)/ Ministry of Internal Affairs and Communications (MIC), Ministry of Justice (MOJ), and Financial Services Agency (FSA)), prefectural governments, municipalities, R&D institutions, and the financial sector. They have been discussing next-generation solar cells to craft the strategy from a wide range of perspectives, including the history of the PV industry, social implementation, introduction potential, construction and installation, the potential of next generation solar cells from the perspective of consumers, potential for overseas deployment, international standardization, supply chain, finance and insurance. Through the Sunshine Project, Japan once boasted the world’s largest production and introduction of c-Si solar cells, but the momentum has since weakened. Looking back on the history of the PV industry, new developments will start to expand the introduction of PSCs and strengthen industrial competitiveness by not limiting the government’s support to technological development, but by working as a trinity to establish mass production technology, improve production systems, and create demand with a group of stakeholders led by METI.

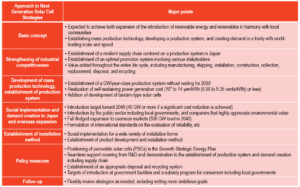

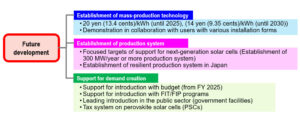

Perovskite solar cells (PSCs) have the potential to overcome various challenges that Japan is currently facing, including the following: 1) introduction in harmony with local communities; 2) reducing the burden on the public; 3) responding to fluctuations in output; 4) accelerating innovation and building a supply chain, and 5) measures to deal with used PV modules. PSCs are expected to be a next-generation growth industry that will play a role in expanding the introduction of renewable energy, providing a stable supply of energy, and strengthening industrial competitiveness. As shown in Tables 1 and Figure 1, the Next generation Solar Cell Strategy consists of the approach to the strategy and its future development. The former will be based on seven perspectives as follows: 1) basic approach; 2) strengthening industrial competitiveness; 3) development of mass production technology and establishment of production systems; 4) social implementation and demand creation in Japan,, and overseas expansion; 5) establishment of installation methods; 6) policy responses, and 7) follow-up, while the latter will be pursued along the three pillars: 1) establishment of mass production technology; 2) development of production systems, and 3) support for demand creation.

The Next-generation Solar Cell Strategy has great significance and progress in that it sets out the target installed capacity by 2040, and the policy of “Team Perovskite Solar Cells Japan,” in which the policy side, the supply side, the utilization side, and the user side play their respective roles to promote the domestic production and introduction of next-generation solar cells in an integrated manner. It will be difficult to achieve the installation of 20 GW if any side is missing. In the production of PSCs, which form the heart of this team, international competition is fierce and the evolution of c-Si solar cells is still continuing, so PSCs are entering an important phase of winning the competition. The key to commercial production is to strengthen and accelerate the technological development framework through the “scale” and “speed” indicated in the strategy. Deliberations are currently underway for the formulation of the Seventh Strategic Energy Plan, and there is a need to significantly expand the introduction of renewable energy toward 2040. PSCs will expand the scope of existing markets and are expected to create new markets such as automotive and agricultural applications, which will provide a basis for raising the target PV installed capacity toward 2040 with both c Si solar cells and PSCs. In order to accelerate the expansion of the introduction of renewable energy, it is necessary to develop this public-private council into a “public-private PV promotion council” as the next step, rather than limiting it to the dissemination of PSCs.

In order to accelerate the expansion of the introduction of renewable energy, it is necessary to develop this public-private council into a “public-private PV promotion council” as the next step, rather than limiting it to the dissemination of PSCs.

Table 1 Approach to Next-Generation Solar Cell Strategy

Source: “Next-Generation Solar Cell Strategy” by METI, compiled by RTS Corporation

Figure 1 Future development of next-generation solar cells

Source: “Next-Generation Solar Cell Strategy” by METI, compiled by RTS Corporation