At the end of 2024, draft proposals for the GX 2040 Vision, along with the Plan for Global Warming Countermeasures and the Seventh Strategic Energy Plan, which will be advanced in an integrated manner under this vision, were compiled. In 2025, these proposals will be approved by the Cabinet, marking the beginning of the latter half of the 2020s as Japan moves toward new targets.

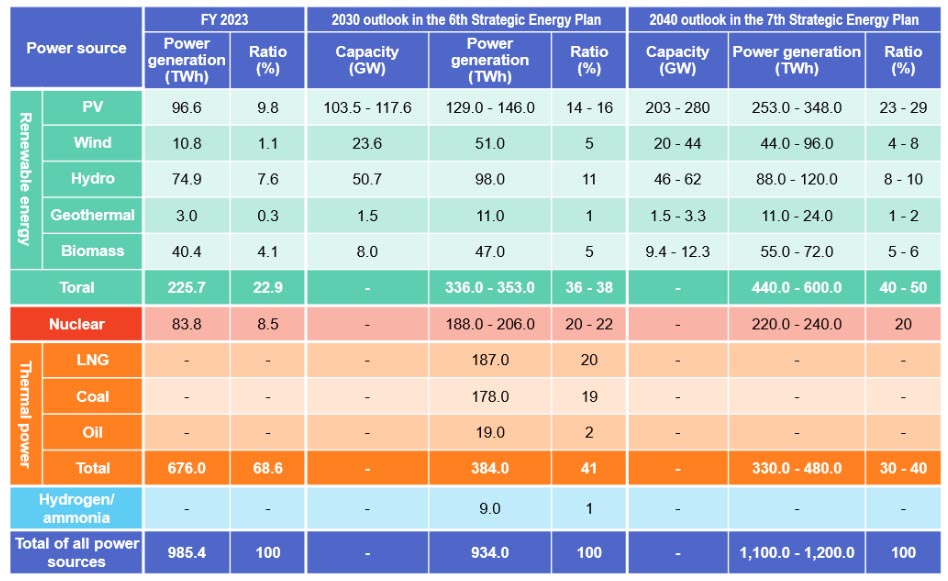

Regarding PV power generation, the 2010s saw an explosive expansion in deployment driven by the start of the Feed-in Tariff (FIT) program, establishing the foundation of today’s market structure, which consists of both the building and non-building sectors. However, since the full sales of PV power allowed for revenue generation through land use, it also led to an Table 1 The projected 2040 energy mix under the draft Seventh Strategic Energy Plan FY 2023 Power source PV Renewable energy Thermal power Wind Hydro Geothermal Biomass Toral Nuclear LNG Coal Oil Total Hydrogen/ ammonia Power generation (TWh) 96.6 10.8 74.9 3.0 40.4 225.7 83.8– Ratio (%) 9.8 1.1 7.6 0.3 4.1 22.9 8.5– under the former FIT program and subsidies provided by relevant ministries and agencies. This led to a decline from the peak level of 10 GWdc to around 5 GWdc. However, the latter half of the 2020s, which is now beginning, is expected to be a five-year period of making a turnaround to expand PV deployment. This is presented in the outlook of the 2040 energy mix of the draft Seventh Strategic Energy increased financial burden on the public and disordered deployment. In the first half of the 2020s, in response to these circumstances, efforts were made to promote the sound expansion of PV power generation. This five-year period focused on creating a business environment for shifting to an independent and full-scale deployment by implementing two key measures: first, establishing new mechanisms and regulations, including the Feed-in Premium (FIP) program, to integrate the market; and second, strengthening business discipline including stricter control measures to ensure harmony with local communities. As a result, the capacity of newly approved projects dropped sharply, and annual PV installed capacity became reliant on commissioning of the approved projects Plan. While emphasizing the balance among various power sources, the 2040 target for PV installed capacity has been set, as shown in Table 1, and PV power generation is positioned as the top power source in terms of both capacity and generation, aligning with the future energy mix envisioned by the International Energy Agency (IEA)

Table 1 The projected 2040 energy mix under the draft Seventh Strategic Energy Plan

©RTS Corporation

*The 2040 capacity is calculated from the electricity generation based on the capacity values adopted in the Sixth Strategic Energy Plan, referenced from the materials of the 47th meeting of the Strategic Policy Committee of the Advisory Committee for Natural Resources and Energy (generation per kW: PV 1,244 kWh, wind 2,160 kWh, hydro 1,930 kWh, geothermal 7,330 kWh, biomass 5,875 kWh).

Source: Based on the materials of the 68th meeting of the Strategic Policy Committee, compiled by RTS Corporation

The significantly higher deployment target for PV power compared to other power sources reflects the recognition of its past achievements and future potential. While the 2030 target for the share of power sources was set at 14% to 16%, the newly established 2040 target was raised, or nearly doubled, to 23% to 29%. This share corresponds to power output of approximately 250 to 350 TWh and capacity of 200 to 280 GWac. Assuming that the 2030 target for PV installed capacity of 120 GWAC is achieved, the installed capacity in the decade ending 2040 would be equivalent to the total installation over the nearly 20 years since the start of the FIT program in 2012. Assuming an installation of 75 GWac by 2024, an additional 125 to 205 GWac will be required over the 15 years from 2025 to 2040, meaning an average annual installation of 8 to 13 GWac, which is equivalent to approximately 10 to 17 GWdc in terms of solar cells.

To achieve the PV installed capacity target, the draft Strategic Energy Plan outlines three key pillars: rooftop PV, ground-mounted PV, and the early social implementation of next generation solar cells. It emphasizes promoting deployment and market formation based on these pillars. The rooftop PV focuses on public and private facilities, and residential buildings. For public facilities, PV systems shall be installed on 100% of the PV installable facilities by 2040. For private facilities, new support measures will be introduced under the FIT and FIP programs to promote the dissemination of ZEBs and self-consumption type PV systems, focusing on enabling the early recovery of initial investments and providing credit support for installers. For residential buildings, the goal of PV installation ratio in newly built homes will be increased to 60% by 2030. For ground-mounted PV systems, local governments will promote the setting of renewable energy promotional areas. For agricultural land, PV systems will be introduced on abandoned farmland where agricultural activities are not expected. On active farmland, the expansion of Agro PV systems will be promoted under the condition that business discipline and agricultural activities are maintained. For airports, roads, railways, ports, and other infrastructure, the introduction of PV systems utilizing these spaces will be promoted. Furthermore, the introduction of ground-mounted systems not using the FIT and FIP programs, will also be promoted through utilization of offsite PPA and such. Regarding the early social implementation of next generation solar cells, establishment of a framework for GW-scale domestic production and demand creation will be promoted in an integrated manner, through the development of perovskite solar cell (PSC) technology with the goal of achieving installation of 20 GW by 2040.

The target PV installed capacity for each relevant ministry, including the Ministry of Economy, Trade and Industry (METI), the Ministry of the Environment (MoE), the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), and the Ministry of Agriculture, Forestry and Fisheries (MAFF), which are responsible for expanding PV power generation, will be determined hereafter. However, it is equally important to recognize that the actual expansion of deployment will be carried out by the PV industry and power consumers. Therefore, it is crucial to set the PV installed capacity target for each market, as mentioned earlier, in conjunction with the perspectives of both parties. The PV industry, entrusted with the role of Japan’s future top power source, must bear the trust and responsibility of contributing to the formation of a decarbonized society and the affordable and stable supply of power. It is time to pave the way for the second phase of large-scale PV deployment that has been unfolding since the introduction of the FIT program.