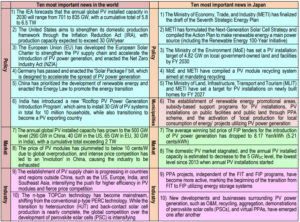

The highlight of PV power generation in 2024, as shown in Table 1, is that the annual global PV installed capacity is expected to reach the 500 GW level. Since reaching a cumulative PV installed capacity of 1 TW in 2022, PV power generation has continued to grow strongly, exceeding the 2-TW mark in just two years, living up to its title as the ‘king’. In particular, expansion of major PV markets is expected as follows: China to 290 GW; USA to 40 GW; European Union (EU) to 65 GW and India to 30 GW. Against this backdrop, the International Energy Agency (IEA) forecasts in its ‘Renewables 2024’ that the annual global PV installed capacity in 2030 will range from 701 to 835 GW, with a cumulative total of 5.8 to 6.5 TW.

Table 1 Ten most important news related to PV power generation in 2024

©RTS Corporation

In terms of policy, the United States has strengthened its domestic PV production framework through the Inflation Reduction Act (IRA), with production capacity expected to exceed 30 GW/year. Support for expanding PV installations has been enhanced in Europe, China, and India.

In the PV industry, intense capital investment by PV module manufacturers has led to an oversupply, causing PV module prices to drop to levels below or at manufacturing costs, falling under 10 cents/watt. As a result of the reevaluation of the supply chain, PV cell/module factories are being planned around the world, starting with the United States, Europe, and India. If this price level continues, PV module manufacturers will start to be eliminated. On the other hand, as the current price level becomes increasingly competitive compared to other power sources, not only will the PV installed capacity per country increase, but it will also spread to all regions of the world.

In Japan, a draft of the GX2040 Vision, which looks ahead to 2040 and significantly impacts the expansion of PV installations, as well as the drafts of the Seventh Strategic Energy Plan and the Plan for Global Warming Countermeasures, were presented. Alongside this, relevant government ministries and agencies as well as local governments advanced measures for renewable energy based on the GX Promotion Strategy formulated in July 2023.

In formulating the Seventh Strategic Energy Plan, the outlook for the 2040 energy mix assumes a power generation amount of 1.1 to 1.2 trillion kWh, with renewable energy accounting for 40~50%, nuclear power for 20%, and thermal power for 30~40%. Renewable energy is positioned as the largest power source, surpassing thermal power. Among renewables, PV power generation is expected to account for approximately 23~29% (equivalent to 202~278GW, with the assumption of 1 kW generating 1,250 kWh/year), making it likely to become the top power source in Japan in terms of both installed capacity and generation amount, surpassing all other power sources (thermal power is not specified by fuel type). The draft of the Plan for Global Warming Countermeasures presented GHG reduction targets of a 60% reduction by 2035 and a 73% reduction by 2040 compared to 2013 levels.

METI enforced the revised Act on Special Measures Concerning Procurement of Electricity from Renewable Energy Sources by Electricity Utilities (Renewable Energy Act) and embarked on strengthening business disciplines aimed at ensuring harmony with local communities in introducing renewable energy. To make renewables a stable power source and to expand the introduction of renewable energy, METI launched the Renewable Energy 100-Year Initiative and announced the Action Plan to make renewable energy a main power source, while also formulating the Next- Generation Solar Cell Strategy to build a domestic PV supply chain.

The Ministry of the Environment (MoE) has continued the Project to promote the Decarbonization Leading Areas (DLAs) and expanded support for the introduction of PV power generation by local governments and private companies. Nine new regions have been added to the DLAs, which have been expanding to a total of 82 regions across 38 prefectures and 108 municipalities, approaching the target of 100 regions. Furthermore, MoE has set a target for local governments to introduce 4.82 GW of PV systems on their owned land and facilities by 2030. In the development of inter-ministerial collaborative policies, MoE and METI formulated a recycling system aimed at mandating the recycling of PV modules, which are expected to be discarded in large quantities from PV power plants. METI and the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) set a FY 2027 target for the installation of PV systems in newly built homes, aiming for 37.5% in newly built detached houses and 87.5% in custombuilt detached houses. Local governments are actively establishing renewable energy promotional areas, implementing subsidy programs for PV installations, introducing PV systems to public facilities through PPA scheme, and promoting ‘local production for local consumption of energy’ projects utilizing PV power generation.

In the market, although the average winning bid price in FIP tenders dropped to 8.17 Yen/kWh (5.21 cents/kWh), the stagnation of new project approvals under the current FIT and FIP programs has continued. While installations supported by subsidies from ministries and agencies as well as voluntary installations independent of the FIT and FIP programs are increasing, start of operation of the approved projects under the old FIT program has significantly declined. Consequently, Japan’s annual PV installed capacity in 2024 is expected to fall to the 5 GWDC level, the lowest since 2013.

In the industry, PPA projects independent of the FIT and FIP programs are becoming more active, and a shift from FIT to FIP with the use of energy storage systems is beginning. New developments and businesses, such as O&M, recycling, aggregation, virtual PPAs, and demonstrations of perovskite solar cells (PSCs), are beginning to emerge one after another.

Japan must use the Seventh Strategic Energy Plan and the new Plan for Global Warming Countermeasures as turning points to halt the decline in PV installations and make 2025 a ‘year of turnaround’ toward increasing the installations once again.