In September 2019, the Ministry of Economy, Trade and Industry (METI) held the first meeting of the Subcommittee on System Reform for Renewable Energy as Main Power Source and started discussions toward a drastic revision of the FIT Act at the end of FY 2020 and reconstruction of renewable energy policy. The Procurement Price Calculation Committee resumed and started discussion on the feed-in tariffs (FIT) for FY 2020 and extension of the PV project capacity range under the tender scheme. As for PV power generation, a policy to realize independence from the current FIT program and to pave the way for integrating the market was presented.

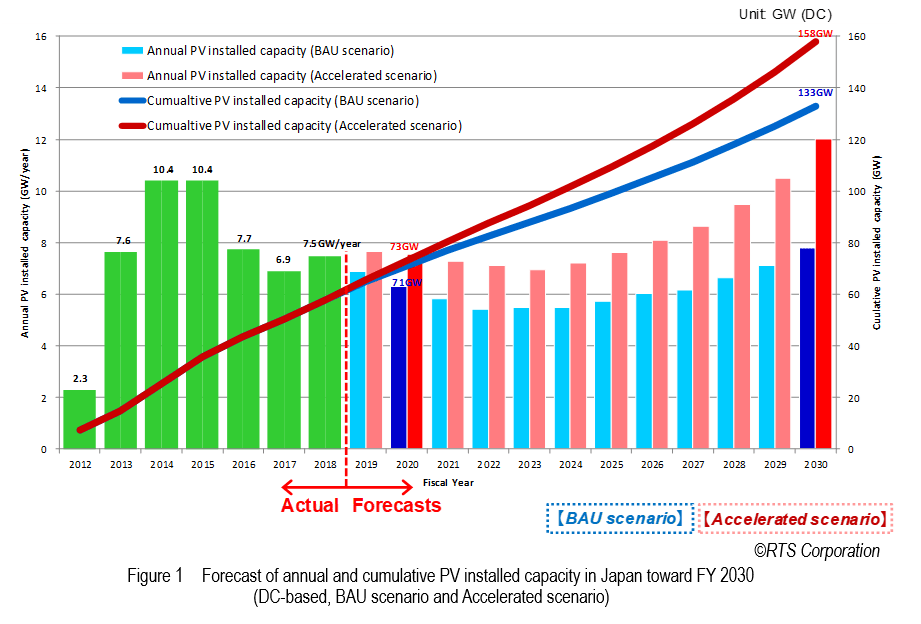

The dissemination of PV power generation in Japan largely grew with the start of the FIT program in July 2012. It is estimated that the cumulative PV installed capacity in Japan as of FY 2018 ended March 2019 exceeded 55 GW (DC-based, the same applies to the following). Reflecting the global prices of PV system installation and based on the premises of expected price reduction of a PV system to around 100 Yen/W ($ 0.926 /W) by FY 2030, RTS Corporation forecasts that the cumulative PV installed capacity in Japan will grow to 130 to 160 GW by FY 2030 as shown in Figure 1, supported by various policy measures toward making PV a mainstream power source, technology development, changes in the installation environment and so on. It is expected that the current Japan’s target PV installed capacity of 64 GW will be achieved by around FY 2020, and it will reach the level of 100 GW by FY 2025. Under the BAU scenario where the installation environment will be improved and technology development will be continued at the same pace as the present, the cumulative PV installed capacity will reach 71 GW by FY 2020 and 132 GW by FY 2030. Meanwhile, under the accelerated scenario of installation and technology development where the governmental ministries and agencies will be fully committed to promoting measures and accelerating technology development toward making PV a mainstream power source, it is expected to reach 73 GW by FY 2020 and 158 GW by FY 2030, driven by growing installation by individuals and industries, expected start of growth of new PV applications including agro-photovoltaics, floating PV (FPV), EV charging, hydrogen production, wall-mounted PV systems and so on in FY 2025 onwards.

In the early 2020s, it is forecast that PV installations taking advantage of the FIT program and the tender scheme will secure certain market shares, whereas installation of storage batteries will expand and the markets of self-consumption and integrated supply/ demand market will grow with new business models such as PV system installation at no initial cost, which will drive the growth of the PV market. By capacity range, < 10 kW PV system market is expected to remain dominated by residential PV systems for both newly-built and existing houses. The mainstream in the ≥ 10 kW PV system market will change to rooftop applications mainly for industrial and public facilities, from ground-mounted MW-scale PV power plants.

This time, in the tender process for ≥ 500 kW PV systems, it was announced that the average successful tender price dropped to 12.98 Yen/kWh (12 cents/kWh) and the top-runner price dropped to 10.5 Yen/kWh (9.72 cents/kWh), respectively. Although there are still divergences between those prices and the international standard prices, the levelized cost of electricity (LCOE) of PV has fallen to a quarter of the LCOE of PV at the start of the FIT program, thanks to the tender scheme, approaching the competitiveness level against conventional energy sources in Japan. METI breaks down the future vision of renewable energy into two categories: 1) “competitive power source” which has potential to grow to the power source with competitiveness and 2) “locally-used power source” which is utilized in local communities. Large-scale PV power plants are classified into the former and residential PV systems and small-scale commercial PV systems are classified into the latter. For residential PV systems and small-scale commercial PV systems, negotiation on grid connection is not complicated, the cost of system equipment and the cost of installation constitute the majority of the cost structure. Therefore, with prospect of further cost reduction in the future, these systems are expected to drive local production for local consumption of electricity as a competitive “locally-used power source”. Under the current FIT program, project development was feasible with strong momentum and velocity based on the “profit endorsed by project approval”. Hereafter, however, project development based on the “competition” is required just like the other ordinary businesses. Looking on the bright side of the drastic revision of the FIT Act in 18 months, the PV business will be able to obtain a significant business opportunity by pursuing both cost reduction to the international level and breakaway from being variable power source.

As a result of the past deployment, PV power generation is consolidating its position as an important energy source for human race in the future and PV dissemination independent from subsidy is expected to be the international standard in the 2020s. Variability, the Achilles’ heel of PV as a power source, can be overcome by integration with electricity storage technology such as storage batteries and sophistication of PV application. If these are realized, PV will become a familiar power source with ability to supply safe and secure energy at low cost. The next decade will bring about dramatic changes to PV over the next ten years.