IEA published “Snapshot of Global PV Markets 2020” and reported that the global annual PV installed capacity in 2019 grew from 103.2 GW in 2018 to 114.9 GW (a preliminary figure). Although the Chinese PV market contracted from 43.4 GW in 2018 to 30.1 GW in 2019, China remained the largest market in the world. What should be noted is that the scale of the global PV market outside of China grew significantly from 58.8 GW in 2018 to 84.9 GW in 2019 and the countries which installed PV are increasing from limited major countries to the whole world. Vietnam and Ukraine newly ranked in and Spain came back to the top ten of installed capacity. The number of the countries which installed more than 1 GW/year increased from 11 in 2018 to 18 in 2019.

The trend of expanding introduction of PV power generation was expected to start in full scale in 2020, since this is the starting year of the implementation of the Paris Agreement. However, due to the rapid global spread of the novel coronavirus (COVID-19) infection, the global economic activities have been driven to the bottom and the expanding introduction of PV power generation is about to be significantly affected as well. Although it was once reported that production had stopped in some part of China which is the world’s supply base of PV products, now it is on the way to recovery. The impact of COVID-19 on PV power generation has shifted from production/ supply to the downstream sector such as distribution and installation works and delays are occurring in project development.

The investment in renewable energy may not increase because of the sharp drop of the crude oil price. However, amid the economic stagnation, we should prepare the countermeasures now, looking ahead to the business environment after the COVID-19 settles down. Since travel is significantly restricted due to the utterly unexpected spread of COVID-19, teleworking and web conferences have become general and social systems such as energy system, industry structure and supply chain as well as lifestyle may possibly change drastically. Depending on the direction of measures for economic recovery which each country will take and the changes in awareness of energy consumers, the trend of decarbonization and the breakaway from dependency on petroleum will be accelerated in accordance with the recovery of energy demand, and the trend of expanding renewable energy use will occur earlier than expected.

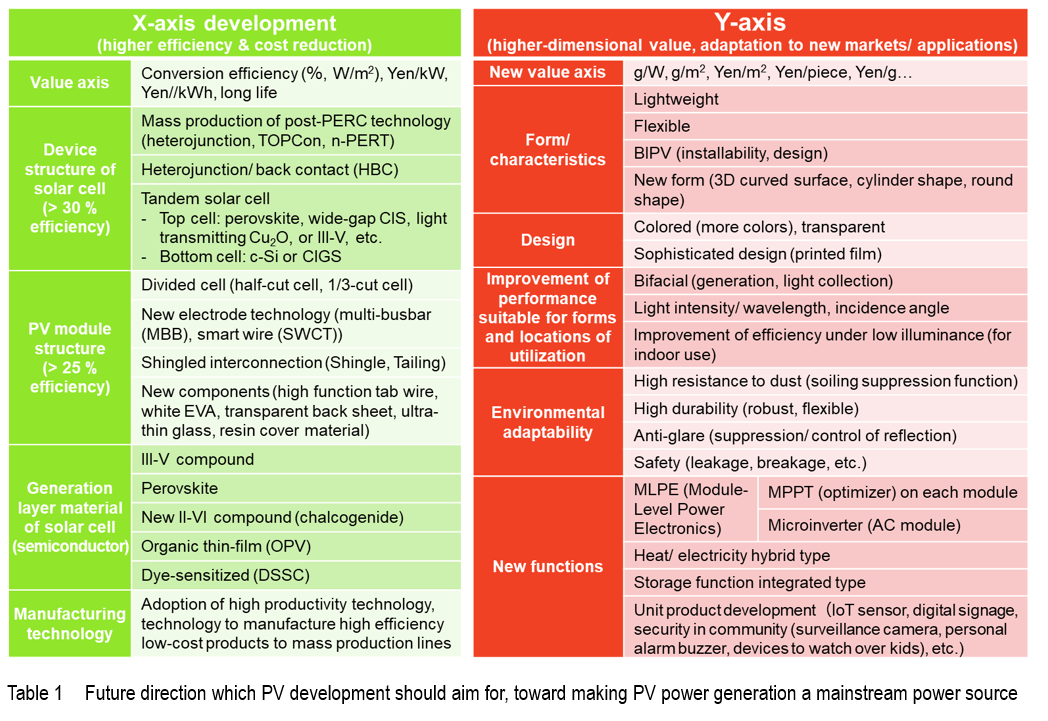

As presented in RTS Monthly Perspective in April 2020 issue of this report, it was expected that the forms of utilizing PV power generation will evolve step by step toward 2050 from PV0.0 to PV5.0 and the direction of technology development of solar cells, the heart of PV power generation is required to be a two-dimensional development of x-axis and y-axis, as indicated in Table 1. Before 2015, when PV was aiming to become a mainstream power source, it was thoroughly required to improve conversion efficiency and to reduce costs as necessary conditions of x-axis. Today, since PV is already positioned as a mainstream power source, the development of y-axis, the pursuit of utilization is required further as sufficient conditions, such as new values, forms, design, high performance, environmental adaptability and functionality.

Having finished PV2.0, the stage of a grid-connected power source, now PV systems are entering PV3.0, the stage of a power source for self-consumption at the price below the power purchase price. The dominant solar cells at this stage are estimated to be crystalline silicon (c-Si) PV modules with the conversion efficiency of over 20 % and most of the products will be produced by Chinese companies. In the 2030s, however, PV will develop to PV4.0 and will play a role as a mainstream power source. At this stage, PV modules will be required to have the conversion efficiency of over 25 % and have functions which correspond to the status of use. Since performance improvement of c-Si technology alone is already at its upper limit, the next generation solar cells may be tandem-type or made of new materials, depending on the progress of the technology development in the future. Aside from the kW-based cost competition, by pursuing y-axis thoroughly and simultaneously, it will be possible to realize addition of various functions which users expect from PV power generation and to create new fields of utilization and markets. Furthermore, when the stage moves to PV5.0, PV systems are required to serve not only as a power source but also as a primary energy to the electrification of the transport sector and heat supply field and various types of solar cell groups will play roles according to the format of use. Such a situation will be realized only when technology development and innovation cooperate with the technologies of industries and fields which use PV power generation. For the development of technologies and products which assume the use of PV power generation, there is a large area which is interlocked with the peripheral field of PV power generation.

Fragmentation of the supply chain caused by the spread of COVID-19 is a huge risk for Japan as a nation. Considering the global development of PV systems and the change of players by innovations in the future, for the manufacture of PV related products, it is necessary to have a new national direction based on the medium- to long-term perspective, to develop high added values which correspond to the changes of the social system and to promote the growth of burgeoning of the next generation PV manufacturing.