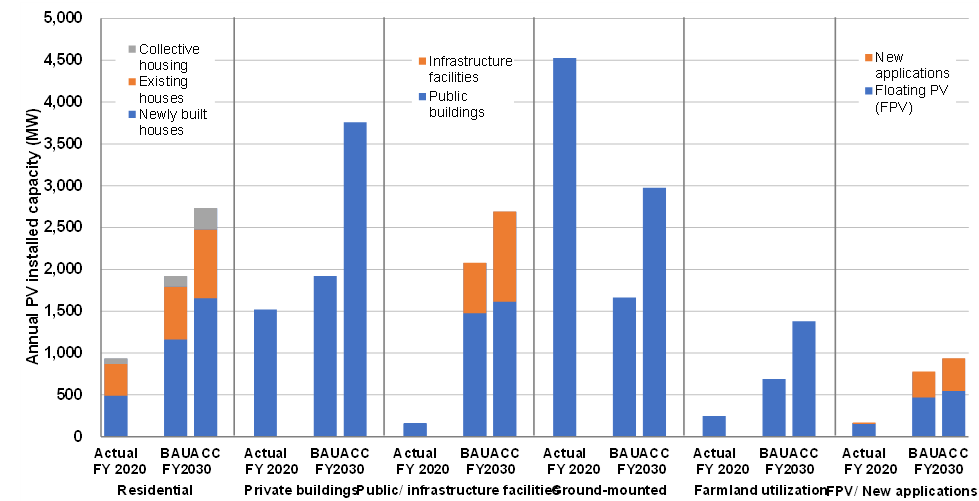

With the start of FY 2022 (April 2022 to March 2023), the Acts for Establishing Resilient and Sustainable Electricity Supply Systems and the revised Law Concerning the Promotion of the Measures to Cope with Global Warming have come into effect and a new market formation for PV power generation has begun. Looking at the outlook for Japan’s PV market by segment under the new dissemination environment, in the residential segment, against the backdrop of rising electricity prices and enhanced resilience, not only will the installation of PV systems for newly-built detached houses as standard equipment be promoted among large- and medium-sized housebuilders and some regional and local construction companies, but ZEH with storage batteries will also expand. After 2025, the revision of the Building Energy Efficiency Act will make it mandatory to comply with energy conservation standards, which will accelerate the introduction of PV power generation. In terms of existing detached houses, the national and local governments’ support for energy-conserving renovation and the introduction of the PPA model which does not require installation costs will spread. Apartment houses (collective housing) will also see progress in the installation of PV systems as standard equipment by major housing manufacturers and rental apartment house manufacturers. Efforts to introduce PV systems to existing apartment houses will also begin, taking advantage of opportunities for large-scale repairs.

In the segment of private facilities (factories, distribution facilities, office buildings, offices, commercial facilities, etc.), against the backdrop of rising electricity prices and enhanced efforts for carbon neutrality, the shift to ZEB and the installation of PV systems as standard equipment will progress for newly-built buildings, while the expansion of introducing on-site PV power generation which use the PPA model will grow for existing buildings. Furthermore, the introduction of PV power generation will be accelerated to expand the procurement of renewable energy electricity to support decarbonized management, corporate value improvement and BCP (Business Continuity Plan). The installation locations for PV systems will diverse further, utilizing parking lots, exterior walls, etc. and the PV installed capacity for a single facility is expected to grow.

In the segment of public and infrastructure facilities, based on the Plan for Global Warming Countermeasures and the Government Action Plan, the prioritized introduction of PV power generation to public facilities will be implemented and more than 50% of public facilities will be equipped with PV systems by 2030.Based on the MLIT Environmental Action Plan, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) will expand the introduction of PV power generation throughout the entire infrastructure facilities; starting with airport facilities, to roads, railroads, public rental housing and parks. In addition, local governments across Japan will also systematically expand the introduction of PV power generation to public facilities and the lands they own.

In the segment of ground-mounted installations, the majority of extra high-voltage projects are the former-FIT-approved projects which have not started operation for a long time, while new projects will be installed based on positive zoning, utilizing previously used land, unused land and public land. In terms of high-voltage projects, introduction will continue based on positive zoning, utilizing previously used land, unused land, vacant lots and public land. In addition to the above, non-FIT/FIP off-site corporate PPAs as well as new-type MW-scale PV projects will emerge such as MW-scale PV projects in harmony with local communities which use self-wheeling and municipal MW-scale PV projects. In terms of low-voltage projects, the development of non-FIT aggregated projects which utilize unused land, vacant lots, parking lots, etc. and FIT projects for local use will continue.

In the emerging segment, the introduction of PV power generation on agricultural land will gradually progress through the establishment of rules for the introduction of PV systems on farmland under the initiative of the Ministry of Agriculture, Forestry, and Fisheries (MAFF) and the benefits of introducing PV systems in agriculture will become more widespread. Meanwhile, the Agricultural Committees under MAFF will facilitate the permission to convert farmland for the installation of PV systems on farmland. Furthermore, the introduction of PV power generation which will lead to the recovery of devastated farmland and the demonstrations of large-scale introduction on farmland will also begin.

In terms of PV system installation on water surface, based on the installation records on reservoirs and agricultural reservoirs, introduction will expand in cooperation with local governments through positive zoning. On the other hand, efforts will be made to enable introduction through the deregulation and the establishment of rules for introduction by the responsible ministries and agencies.

Based on the above outlook of PV installations by segment, as shown in Figure 1, the market size forecasts are based on two scenarios, BAU scenario and Accelerated scenario. The BAU scenario assumes the continuation of the current growth that the installation target in the Sixth Strategic Energy Plan will be achieved and the Accelerated scenario assumes the accelerated introduction that there will be a significant improvement of the installation environment and a speedy increase in self-sufficiency rate. The well-balanced market will be formed with the significant growth of the supply-demand integrated market for houses, private facilities and public/infrastructure facilities which will take the place of the ground-mounted installations that have driven the market up until today mainly with the installation of MW-scale PV projects, as well as with the emergence of new markets such as the installations on farmland and water surface.

In order to facilitate the smooth formation of such a new PV market, in addition to the cost reduction of PV systems and storage batteries and the development of business models such as PPA, the spread of PV power generation in harmony with local communities through positive zoning and the early resolution of grid and location restrictions by strengthening policy measures led by the responsible ministries and agencies will be required as prerequisites. Therefore, for the formation of the market, it will be even more important to clarify the role sharing and drastically intensify efforts by the whole nation. Japan should lead the world in forming a PV market that can accelerate the pace of the market development, with a view to 2030 and beyond.

Figure 1 Forecasts of PV installed capacity in Japan by market segment (DC-based)

©RTS Corporation